February 29, 2024

February 29, 2024

Commentary

Monthly commentary discusses recent developments across the Ninepoint Diversified Bond, Ninepoint Alternative Credit Opportunities and Ninepoint Credit Income Opportunities Funds.

Economics

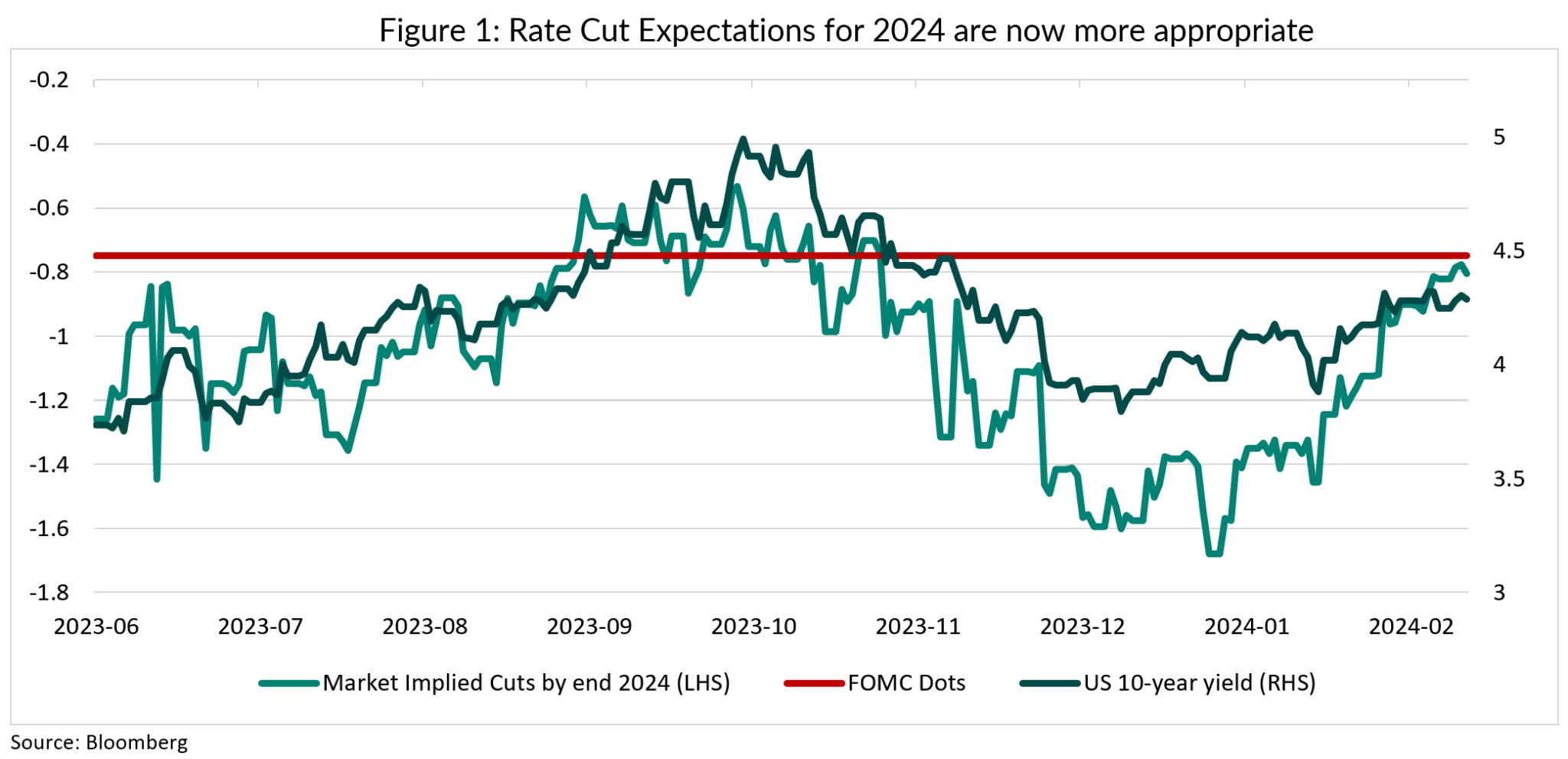

Last month, we made the point that market expectations for rate cuts this year were still unrealistic, and that given the current growth and inflationary dynamics, rate cut expectations needed to be both pushed out in time and reduced in magnitude. As of the end of February, with only about 3 full cuts expected for 2024 in both Canada and the U.S. (same as the Fed’s guidance), we feel like expectations are much more reasonable. (Figure 1).

That still doesn’t mean rate cuts are a certainty for 2024. For example, elevated fiscal spending could keep the economy too hot and prevent any further progress on inflation, preventing central banks from cutting at all. While this isn’t our base case, it is clearly a risk, particularly in the U.S., where the Federal Government is eyeing additional fiscal measures.

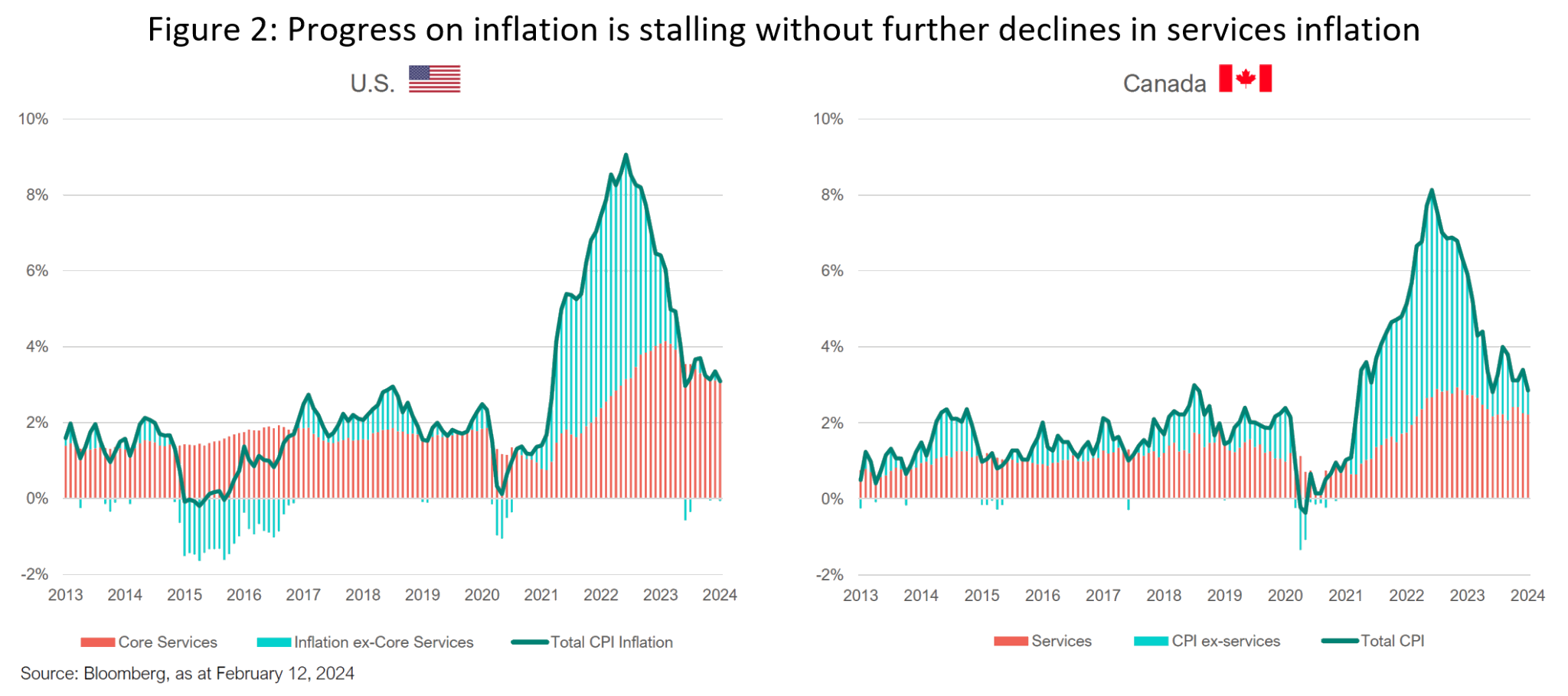

But even without additional fiscal easing, the fight against inflation isn’t over, and it would be foolish for the Fed or the BoC to declare victory. Most of the decline in inflation over the past two years can be attributed to declines in energy and goods prices, whereas services inflation continues to run at very elevated levels. To illustrate this dynamic, we show in Figure 2 below the contribution of goods (blue) and services (red) to inflation. To achieve a level of services inflation consistent with both central bank’s 2% inflation target, we need to see the contribution of services inflation (about 50% of the CPI basket) decline by around a half of where it currently is.

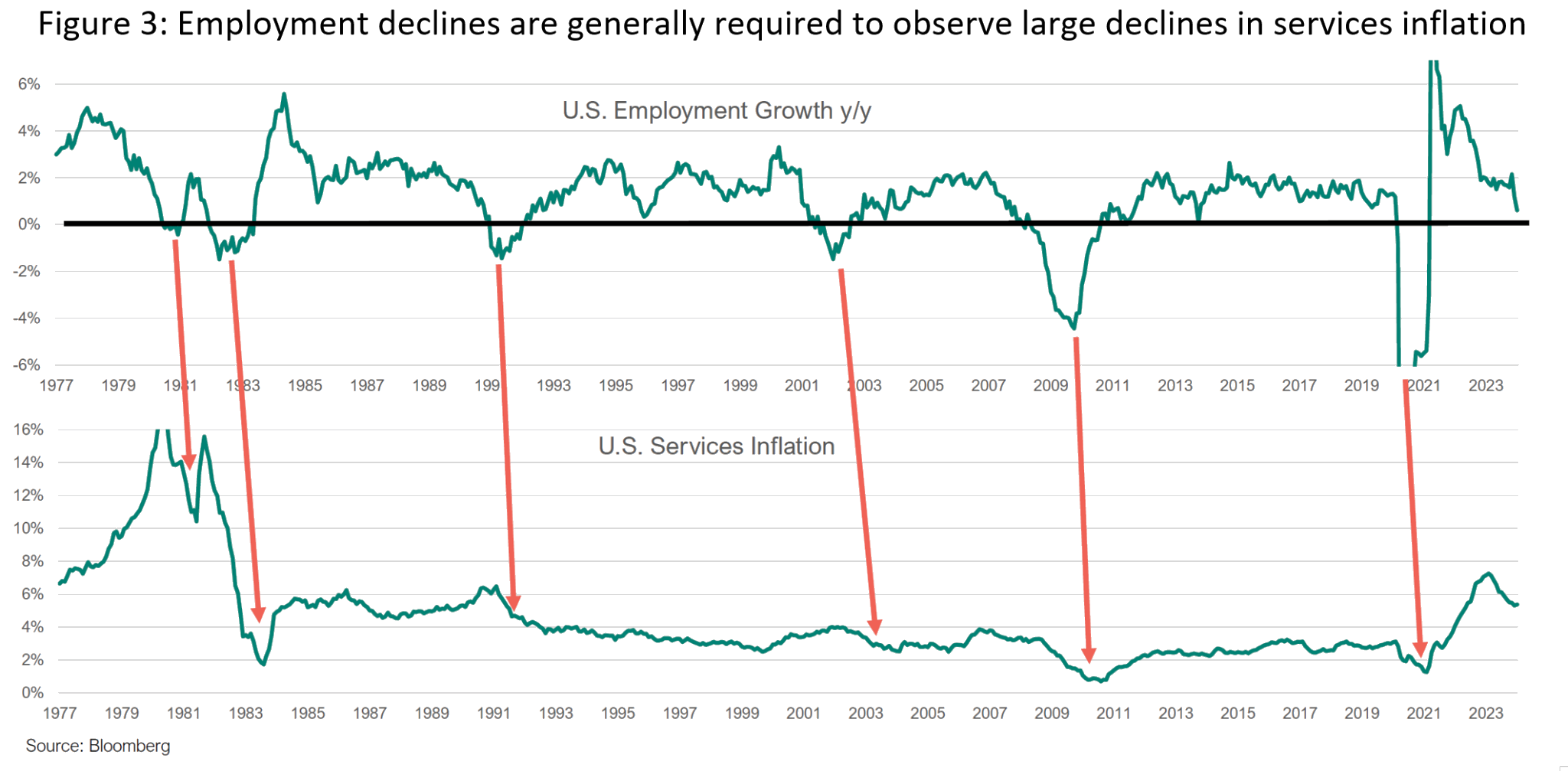

What is services inflation, and why isn’t it declining the same way goods and energy prices are? About half of services inflation is the cost of shelter, and the rest are services like health care, education, transportation, etc. Those services (construction included) are generally labour intensive, and therefore are more directly related to the state of the labour market. That relationship can be seen in Figure 3 below, where we show the annual growth rate in employment (i.e. the yearly % change in the number of employed people) and services inflation.

We show U.S. data here because the availability of data is extensive, allowing us to go back to the 1970s. The data is clear: for the last 50 years, there hasn’t been a meaningful and rapid decline in U.S. services inflation that wasn’t preceded or coincided with a shrinking of the labour market (i.e. job losses).

A weaker labour market will allow wages to decline, prices to drop, and eventually also feed into the housing market, where we need to see further softening. There is no such thing as immaculate disinflation. The pandemic created imbalances in the supply and demand of goods, and that is now a thing of the past (as the blue bars in Figure 2 illustrate), but the cyclical excesses of services inflation cannot be resolved until the labour market cracks. If the Fed and the BoC cut too soon, before services inflation has been properly tamed, they risk seeing a resurgence in inflation, which would require them to hike again. At this juncture, if the labour market doesn’t deteriorate, we should expect fewer interest rate cuts for 2024. And a very slight possibility of no cuts – remember 2023.

Credit

Canadian investment grade credit spreads continued their march tighter in February rallying 10bps in the month. That is an impressive month on a stand-alone basis, but also because supply was robust and US spreads ended the month flat. Canadian corporate bond supply in February was $12bln, the second highest February on record and follows a record January. What is even more impressive is that issuers rarely had to pay new issue concessions which speaks to the strong appetite for corporate bonds YTD. Given that US credit sold off 10bps heading into month end on supply indigestion (record issuance YTD there as well), we expect Canadian credit to follow suit (it normally does with a lag). Perhaps the lack of spread compression, post issuance in some of the more recent deals is a clue of what is to come.

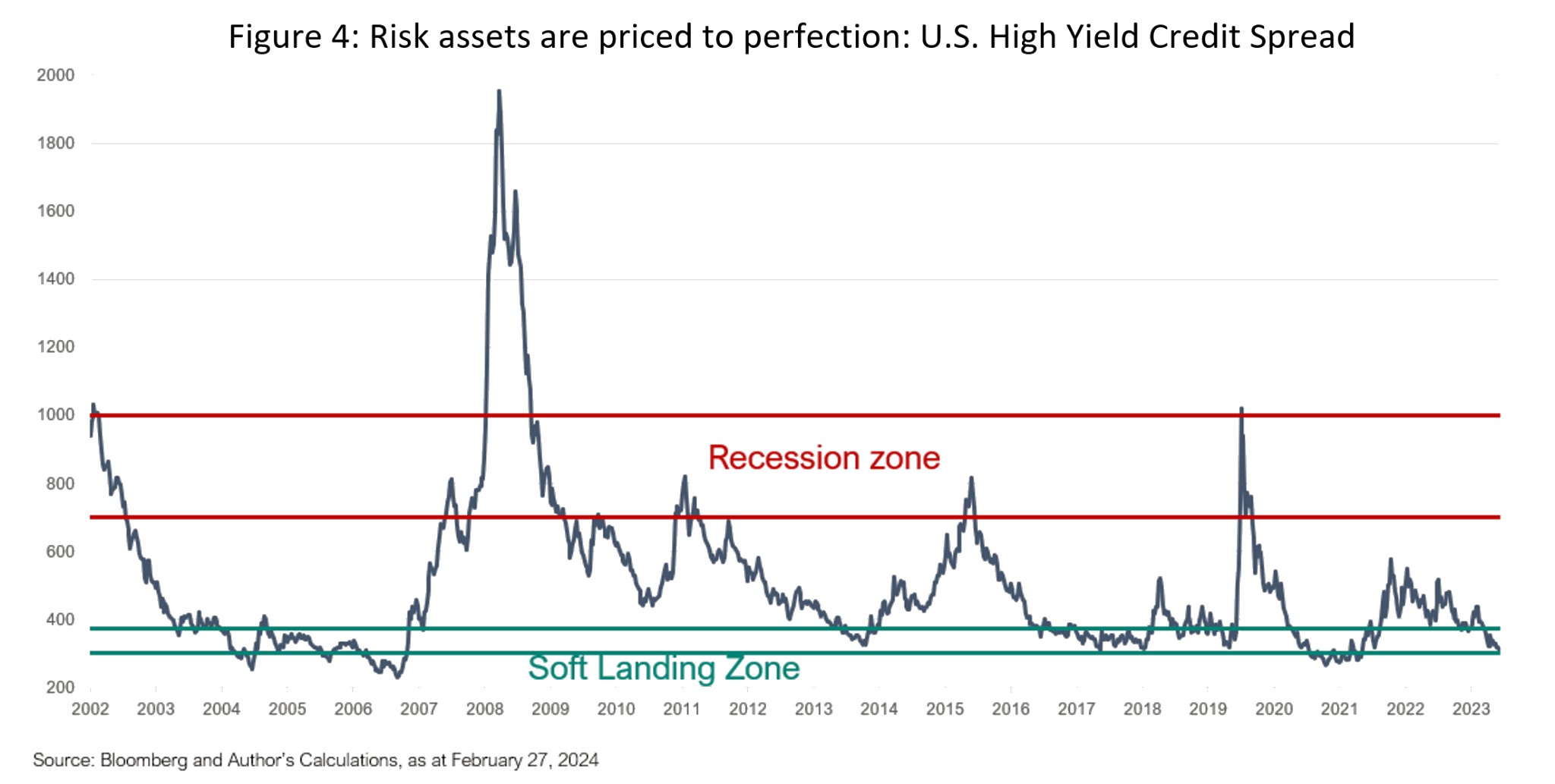

After this fast and furious rally, with very few exceptions, credit is now priced to perfection. For example, HY spreads (Figure 4) are now back to 2021 levels, last seen when we had QE, fiscal stimulus, 0% interest rates, and very few defaults. Across the funds, we are much more defensively positioned across credit products, focusing on higher quality issuers, and shorter maturities to minimize volatility.

Individual Fund Commentary

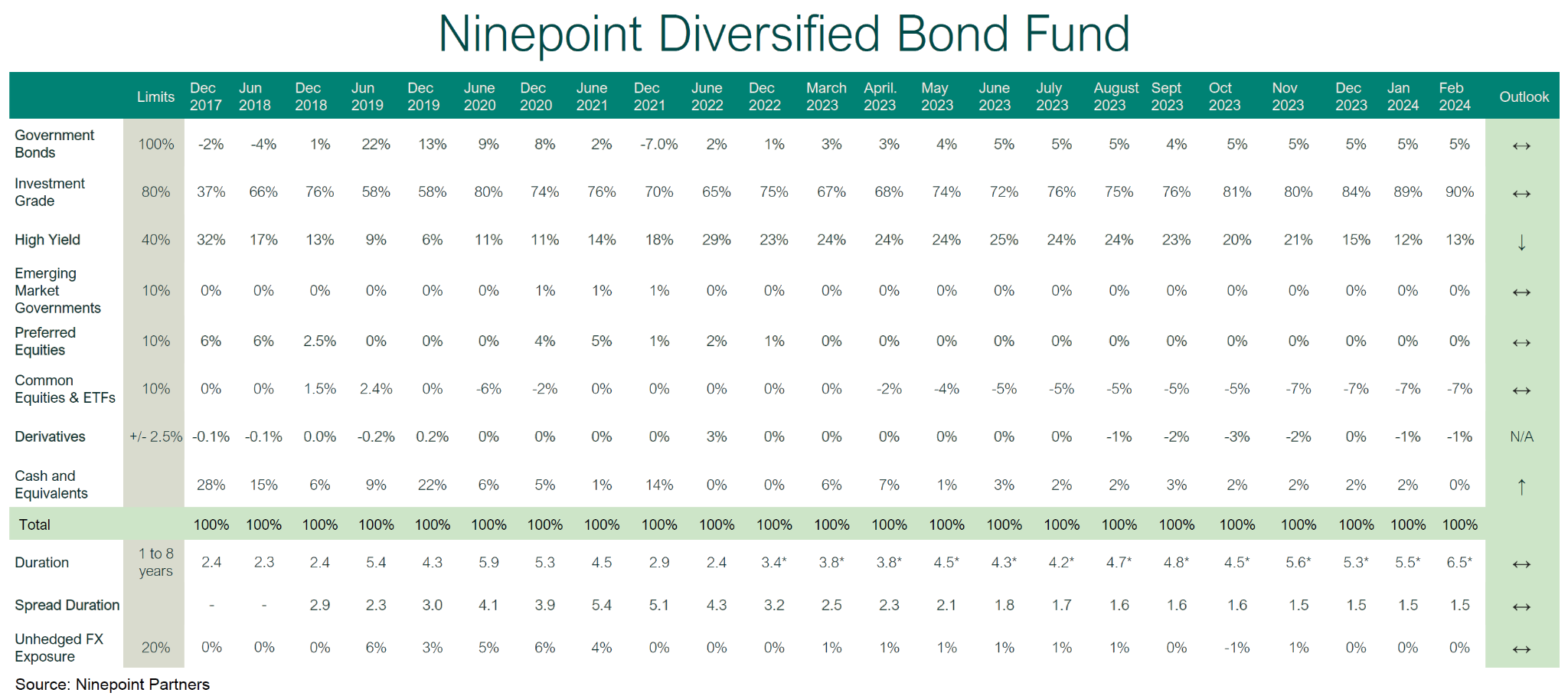

Ninepoint Diversified Bond Fund

The fund remains defensively positioned with a focus on short-term investment grade bonds. Our High Yield weight moved up month-over-month from 12% to 13%, due to new issue activity. Maturities at the beginning of March will ensure a continued decline in our HY weight. The average credit quality remains at BBB+ which we feel is prudent given our macro-economic outlook. The yield-to-maturity of the fund moved down 10bps month-over-month and now sits at 7.5%. Given the sell-off in rates, we increased duration by one year and now sits at 6.5 years. Lastly, our short position in HY (used for credit hedging purposes) remains at our target of -7%.

Ninepoint Alternative Credit Opportunities

The fund remains defensively positioned with a focus on short-term investment grade bonds. Our High Yield weight moved up month-over-month from 10% to 12%, due to new issue activity. Maturities at the beginning of March will ensure a continued decline in our HY weight. The average credit quality remains at BBB+ which we feel is prudent while leverage remains historically low (by our standards) at 0.7x. The yield-to-maturity ended the month at 8.6% while duration ended the month at 3.4 years (up from 3 years) with the sell-off in rates. Our short position in US High Yield ETFs (HYG and JNK used for credit hedging purposes) remains at our target of -11%.

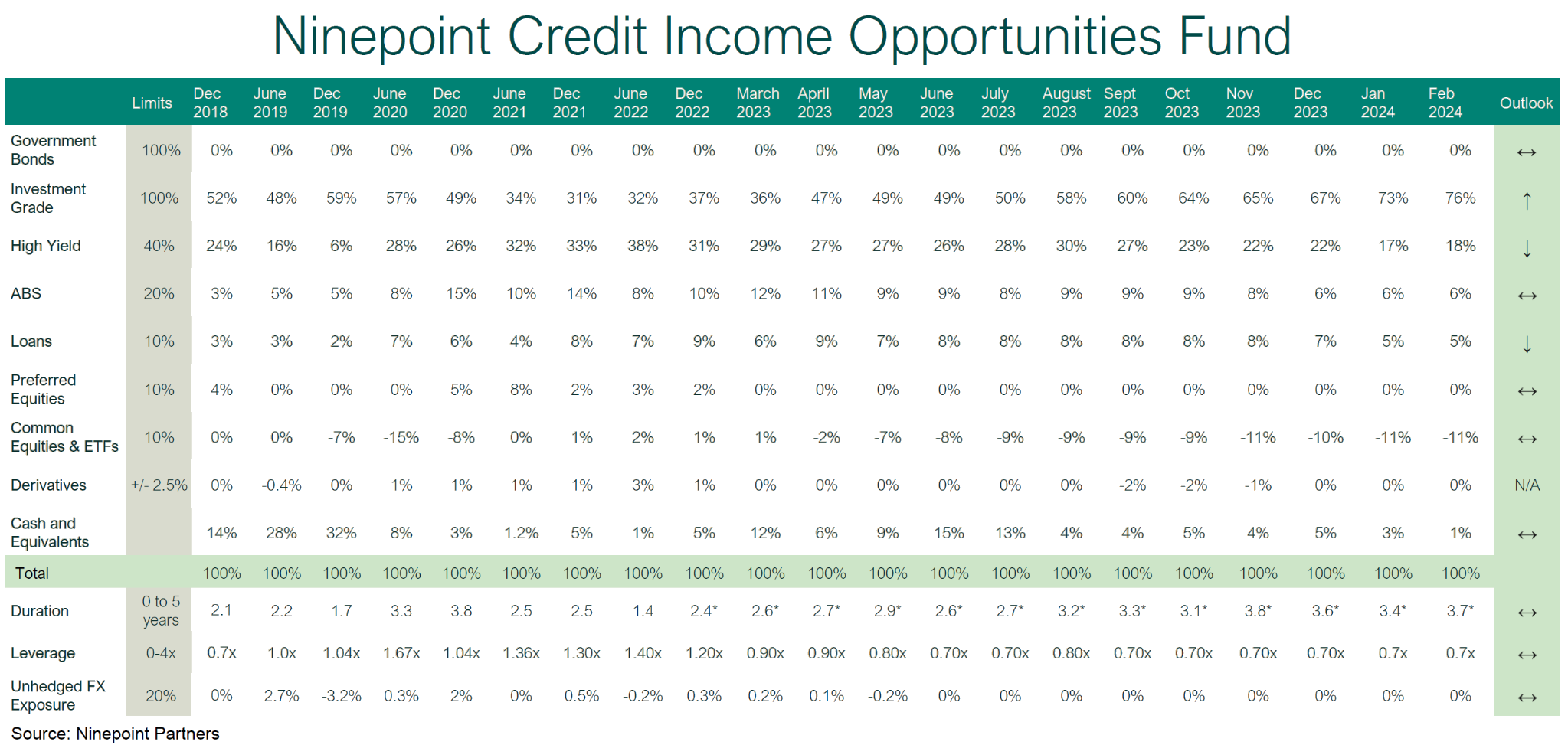

Ninepoint Credit Income Opportunities

The fund remains defensively positioned with a focus on short-term investment grade bonds. Our High Yield weight moved up month-over-month from 17% to 18%, due to new issue activity. Maturities at the beginning of March will ensure a continued decline in our HY weight. The average credit quality remains BBB which we feel is prudent, while leverage remains historically low (by our standards) at 0.7x. The yield-to-maturity ended the month at 9.3% while we moved duration 0.3 years higher to 3.7 years given the sell-off in rates. Our short position in US High Yield ETFs (HYG and JNK used for credit hedging purposes) remains at our target of -11%.

Conclusion

This year is like a game of chicken between central bankers and the market. Who will blink first? As the adage says: “Don’t fight the Fed”. We won’t. And if we can keep earning such elevated yields on high quality short term paper for a bit longer, all the better.

Mark, Etienne & Nick

Ninepoint Partners