November 30, 2024

November 30, 2024

Commentary

Monthly Update

Year-to-date to November 30, the Ninepoint Focused Global Dividend Fund generated a total return of 31.37% compared to the S&P Global 1200 Index, which generated a total return of 29.36%. For the month, the Fund generated a total return of 7.19% while the Index generated a total return of 4.30%.

Ninepoint Focused Global Dividend Fund - Compounded Returns¹ As of November 29, 2024 (Series F NPP964) | Inception Date: November 25, 2015

1M |

YTD |

3M |

6M |

1YR |

3YR |

5YR |

Inception |

|

|---|---|---|---|---|---|---|---|---|

Fund |

7.2% |

31.4% |

10.9% |

18.0% |

33.8% |

12.5% |

11.9% |

9.9% |

S&P Global 1200 TR (CAD) |

4.3% |

29.4% |

7.9% |

13.7% |

31.8% |

12.5% |

13.9% |

12.4% |

As we approach the holiday season and the end of 2024, investors should be pleased with their returns for the year. Further, although we are already part way through December, we are entering what has historically been a seasonally strong period for the equity markets, especially after excellent year-to-date performance. We think that the themes and trends that have been working are likely to persist through the balance of the year and into early 2025, as investors chase performance while refraining from selling winners to avoid realizing taxable capital gains.

The first week of November has really set the stage for this outcome, with two key catalysts occurring over the span of just three days. The most important catalyst was obviously the US Presidential Election on November 5th, and the Trump victory coupled with the Republican Party’s sweep of Congress was well received by the equity markets. The investment themes that subsequently outperformed were the same as the ones that had worked after the 2016 election and were tied to deregulation, lower taxes and economic growth. Conversely, stocks exposed to the threat of tariffs on foreign-produced goods and almost every stock related to renewable energy production dramatically underperformed.

We think that the themes and trends that have been working are likely to persist through the balance of the year and into early 2025

The second key catalyst, the US FOMC meeting on November 7th, was almost lost in the election noise but the Committee did announce its second rate cut of the cycle, lowering the overnight rate by 25 basis points to 4.75%. However, the odds of another 25-bps cut in December have subsequently fallen and the number of expected interest rate cuts in 2025 have declined from four to just two, as the economy has remained robust, and the labour market has remained firm. The rationale for fewer interest rate cuts going forward is also based on the fact that President Trump’s policies (primarily aggressive fiscal spending and tariffs on foreign-produced goods) are considered broadly inflationary, but we would like to take a wait-and-see approach before making judgement because some of the President-elect’s other policies may prove deflationary (further, it remains to be seen what will ultimately be enacted). In the meantime, the prospect of generally lower interest rates remains supportive for the equity markets through the easing cycle as long as the economic data does not deteriorate significantly from here.

Into 2025, we are optimistic for continued positive equity performance, but we think that there is the potential for a brief period of weakness at the beginning of the year. Conceptually, portfolio rebalancing after year end may create some weakness at the index level, as investors rotate out of the largest mega cap growth companies into the more undervalued, cyclical parts of the market. We think that the growth rate differential between the Mag7 and the rest of the market should converge more significantly in 2025, which would provide some support for this trade. But broadly speaking, with S&P 500 consensus earnings estimates rising through 2024, and currently at $280 for 2025 and $305 for 2026 (according to LSEG), we still think equity markets will post solid gains in 2025.

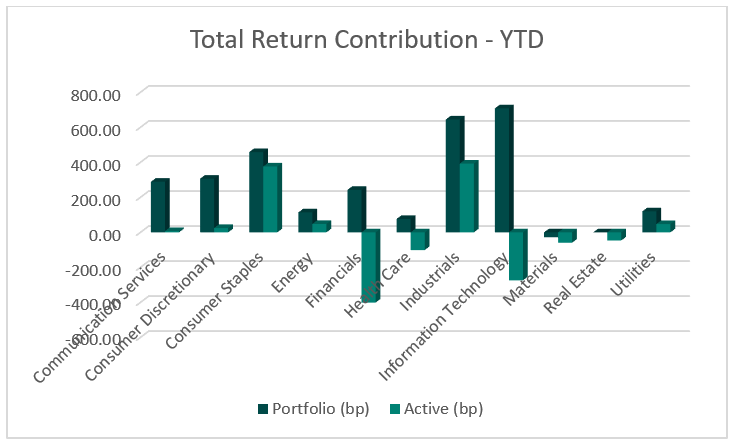

Top contributors to the year-to-date performance of the Ninepoint Focused Global Dividend Fund by sector included Information Technology (+708 bps), Industrials (+645 bps) and Consumer Staples (+458 bps), while only the Materials (-28 bps) sector detracted from performance on an absolute basis.

On a relative basis, positive return contributions from the Industrials (+393 bps), Consumer Staples (+376 bps) and Energy (+48 bps) sectors were offset by negative contributions from the Financials (-401 bps), Information Technology (-274 bps) and Health Care (-101 bps) sectors.

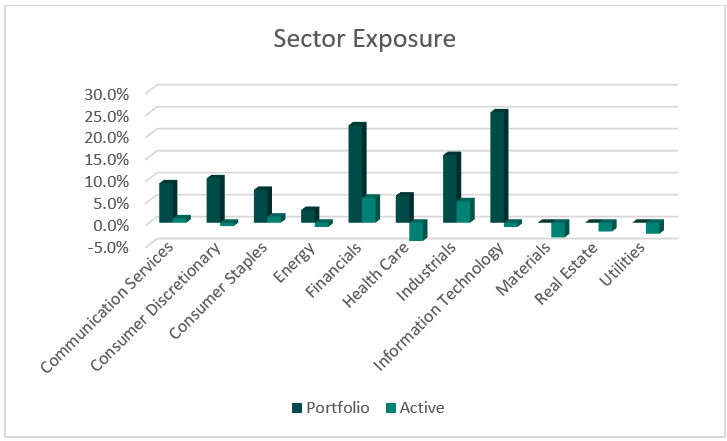

We are currently overweight the Financials, Industrials and Consumer Staples sectors, while underweight the Health Care, Materials and Utilities sectors. With the US Presidential Election behind us and monetary policy easing underway, we are optimistic over the balance of the year and into 2025. However, we will be carefully watching for policy announcements from the incoming President’s administration and the ensuing impact on growth and inflation. The key question for the equity markets in 2025 will be whether President Trump’s policies prove inflationary, thus creating a spike in bond yields and necessitating a pause in the monetary policy easing cycle. In the meantime, we remain focused on high quality, dividend payers that have demonstrated the ability to consistently generate revenue and earnings growth through the business cycle.

The Ninepoint Focused Global Dividend Fund was concentrated in 30 positions as at November 30, 2024 with the top 10 holdings accounting for approximately 38.1% of the fund. Over the prior fiscal year, 21 out of our 30 holdings have announced a dividend increase, with an average hike of 6.1% (median hike of 4.3%). We will continue to apply a disciplined investment process, balancing various quality and valuation metrics, in an effort to generate solid risk-adjusted returns.

Jeffery Sayer, CFA

Ninepoint Partners