February 28, 2025

February 28, 2025

Commentary

Monthly Update

We have just passed the one-year anniversary of the Canadian Large Cap Leaders Split Corp and can now finally begin reporting performance stats1. For the trailing one-year period, ending February 28, the Canadian Large Cap Leaders Split Corp Class A Shares generated a total return of 26.36% and the Preferred Shares generated a total return of 7.74%. For the month, the Class A Shares generated a total return of 0.48% while the Preferred Shares generated a total return of 0.62%. We are very pleased with these initial performance results and believe that the IPO of the Split Corp was extremely well-timed for long-term gains.

CANADIAN LARGE CAP LEADER SPLIT CORP. - COMPOUNDED RETURNS¹ AS OF FEBRUARY 28, 2025 | INCEPTION DATE: FEBRUARY 22, 2024

1M |

YTD |

3M |

6M |

1YR |

Inception |

|

|---|---|---|---|---|---|---|

Canadian Large Cap Leaders Split Corp - Class A Shares |

0.48% |

2.87% |

2.87% |

2.87% |

26.36% |

24.79% |

Canadian Large Cap Leaders Split Corp - Pref Shares |

0.62% |

1.25% |

1.25% |

1.25% |

7.74% |

7.75% |

Unfortunately, the euphoria after President Trump’s victory and hopes of “animal spirits” powering North American markets to new highs have quickly faded. The Trump administration’s instigation of a global trade war, premised on irrational arguments and questionable legality, has disrupted and destabilized the markets with inherently conflicting and economically unsound policies. From our perspective, it seems clear that the uncertainty will be much higher over the next four years than over the past four years. The threat of tariffs applied to goods imported from Canada, Mexico and China to the United States will likely act as an overhang on investor sentiment, with potentially on-again/off-again announcements adding to the confusion.

In this environment, we remain invested in a diversified portfolio of high-quality, dividend-paying Canadian companies while we wait for the stock markets to stabilize. Thankfully, the net asset value of the Class A shares of the Canadian Large Cap Leaders Split Corp remains significantly above the split-adjusted IPO price and the outlook for the portfolio remains solid. Again, we expect that interest rates will continue moving lower in Canada, making our holdings even more attractive from a yield perspective.

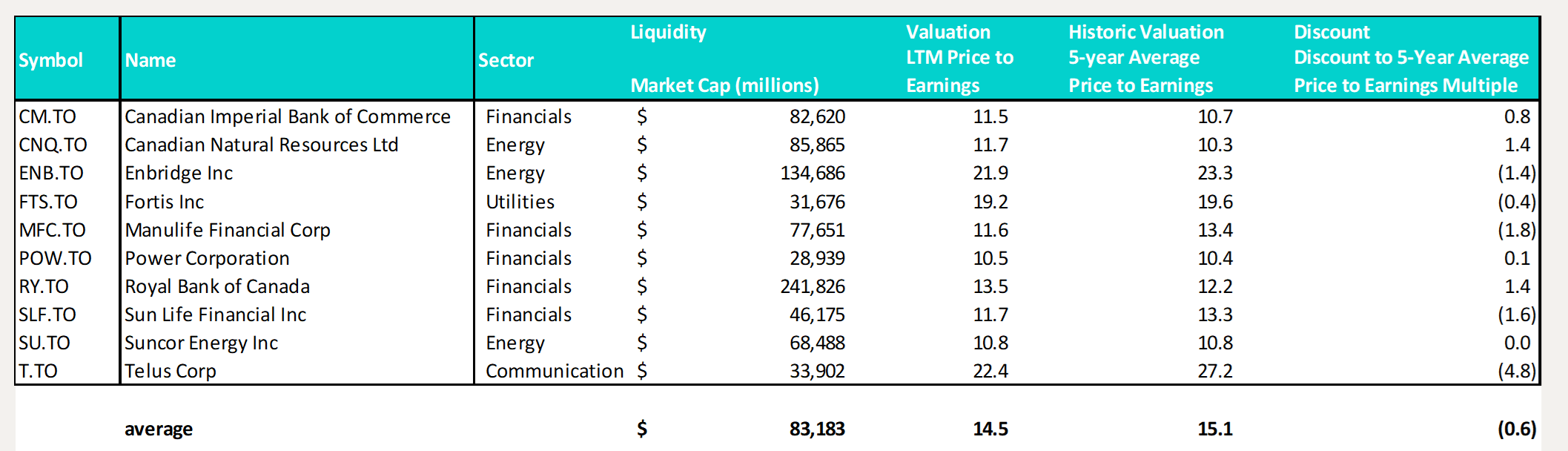

Information below is specific to individual securities held in the Portfolio. It is only intended to describe key characteristics of individual holdings at a point in time and makes no inference about the return nor yield of either the Preferred Shares or the Class A Shares of the Canadian Large Cap Leaders Split Corp.

From the chart above, we can see that our holdings, on average, trade at an LTM price to earnings multiple of 14.5x, compared to the 5-year average price to earnings multiple of 15.1x. However, given our outlook for lower interest rates (and supported by a significant discount to the S&P 500, which currently trades at about 20.7x forward earnings, according to FactSet), multiples still have plenty of room to expand in Canada. Further, with the Class A Shares trading approximately 13% below the reported NAV at the close on February 28, 2025, we can adjust this table to visualize the implied valuation today:

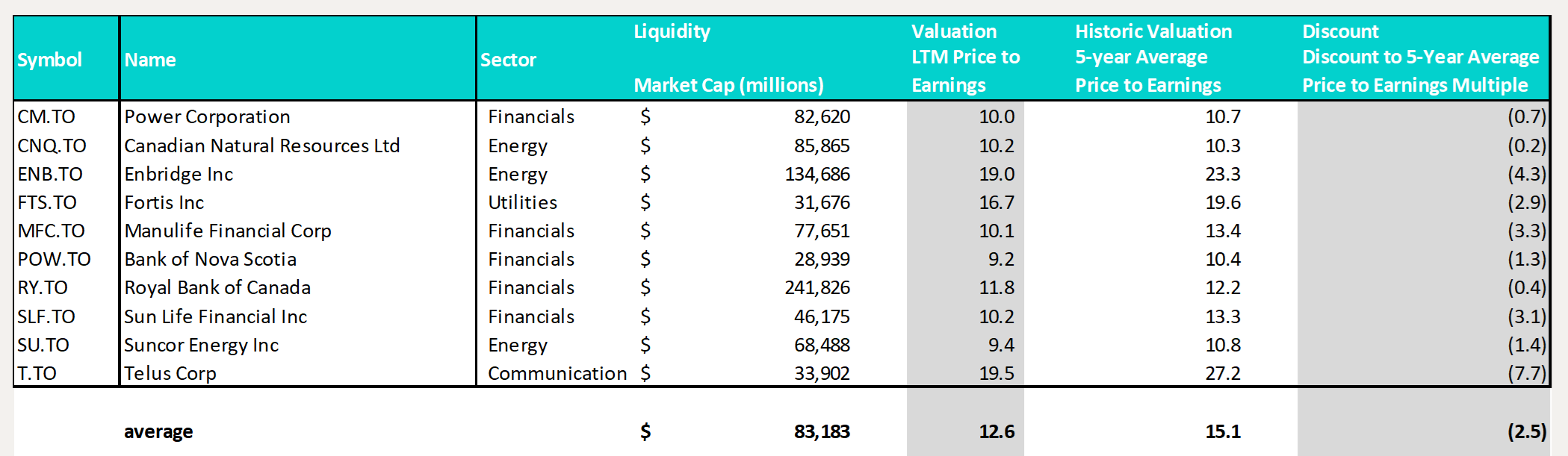

Information below is specific to individual securities held in the Portfolio. It is only intended to describe key characteristics of individual holdings at a point in time and makes no inference about the return nor yield of either the Preferred Shares or the Class A Shares of the Canadian Large Cap Leaders Split Corp.

The implied discount was currently 2.5x worth of multiple points at the close on February 28, 2025, which highlights the opportunity to buy our portfolio of Canadian high-quality, dividend payers significantly below long-term historic valuations through the purchase of shares of NPS on the open market.

Because we have been quite disappointed with the persistent trading discount, we recently completed a Class A Share split, while maintaining the same distribution amount per share, and a concurrent private placement of Preferred Shares. We hoped to reward Class A shareholders with more stock, increase the dollar amount of distributions paid to each Class A by approximately 15%, increase the yield on each Class A share (currently approximately 13%) and theoretically improve trading liquidity. While it is still reasonably early after completing the split and stock market volatility has picked up, we are optimistic that the Class A shares will trade closer to net asset value over time.

Finally, we would like to highlight that the Canadian Large Cap Leaders Split Corp has announced its next distribution, payable on March 14, 2025, to Class A Shareholders of record at the close of business on February 28, 2025. As planned, holders of the Class A Shares will receive the $0.12500 per share regular monthly dividend.

Until next month,

John, Jeff & Colin

Ninepoint Partners

1All returns are based on Net Asset Value per Class A share, or the redemption price plus accrued interest per Preferred share and assumes that distributions made by the Fund on the Class A shares, or Preferred shares in the period shown were reinvested in additional Class A shares and Preferred shares of the Fund as at 2/28/2025.