|

|

|

|

(7 Day Change as of April 11, 2025 11:00AM ET)

|

Bitcoin Price: $82,008

(0.69%)

|

|

DeFi Total-Value-Locked: $88.6B

(5.42%)

|

Ethereum Price: $1,557

(12.97%)

|

|

Crypto Market Cap: $2.60T

(1.14%)

|

Bitcoin Range: $74,727 - $84,360

|

|

TKN.U Close: $11.96 (as at Apr 10, 2025)

|

Ethereum Range: $1,397 - $1,824

|

|

|

Bitcoin Dominance: 62.60%

0.97%

|

|

|

|

|

|

|

Trump Tariff Whiplash Rocks Markets. What’s Next?

|

President Trump’s “Liberation Day” turned into liquidation day, as markets plunged, fear gripped investors, and worries grew in the days that followed that the tariff tantrum could snowball into a financial contagion.

After a week of carnage following Trump’s seeming act of national economic seppuku, it appears the president has finally said Uncle! On Wednesday, Trump

announced

a 90 day pause on the country specific ‘reciprocal’ tariffs. Notably, industry specific tariffs and the baseline 10% reciprocal tariff will remain in place. Trump also ratcheted up pressure on China – increasing tariffs to 145%.

The market reaction to this pivot was euphoric, with the tech-heavy NASDAQ soaring 10% on Wednesday - its biggest daily gain since October 2008. This should serve as a cautionary reminder that the biggest rallies often happen in downturns. To wit, during the great financial crisis, markets resumed their tailspin after the October bounce, and didn’t bottom until March of 2009 – six months later. And Wednesday’s move was followed by another steep down day.

So, what happens next?

For starters, the pivot will ease pressure on the Federal Reserve, America’s central bank. Chairman Jerome Powell will no longer be forced to consider a showdown with the President and an inevitable fight over Fed independence

. It also shifts some of the focus off Republicans in congress, who would have needed to build on their razor thin majority rebuking the president for his Canada tariffs, breaking with the president en masse to build a veto-proof majority. Hell freezing over is a more likely outcome.

So, we’ve stepped back from the cliff’s edge but we’re not out of danger yet.

Trump is only pausing country-specific reciprocal tariffs, while maintaining 10% baseline tariffs and industry specific tariffs. The country specific tariffs could be reinstated at Trump’s whim. In a note to clients, Goldman Sachs

said

they also expect more industry specific tariffs to come, such as on the pharmaceutical industry. With earnings season around the corner, we’re about to get some colour from corporate America’s top executives on what all this uncertainty means for their businesses and the economy. The words unprecedented, uncharted territory, once-in-a-century, suspending guidance, and force majeure will be on my Bingo Card.

Trump’s supporters have been twisting themselves in knots trying to justify his actions. Some claim this is part of some grand strategy to push treasury yields lower so the government can refinance its debt at a cheaper rate. But rates are higher now than before. Then they pivoted, saying tariffs are about shrinking the deficit. But even an optimistic

estimate

of $700 billion in annual tariff revenue is a pittance compared to the government’s estimated $7.3 trillion

spending plan.

What’s more, is $700 billion a year really worth it when you’ve wiped out $10 trillion in wealth, alienated your allies and pushed the economy to the brink of a recession?

And if tariffs are such a great source of revenue, then why is the White House

clamoring

to reach ‘phenomenal deals’ with 50+ countries that would see tariff barriers lifted?

So, now the new rationale: Trump is playing “4-dimensional chess” and will isolate China through bilateral agreements and so-called friend-shoring of manufacturing to friendly countries, specifically Mexico and Canada.

Come again? Mexico and Canada were the first countries to provoke Trump’s ire in his second term. And the president put tariffs on everyone including the remote Antarctic Heard and MacDonald Islands, whose only inhabitants

are

penguins. What’s more, those worldwide ‘reciprocal’ tariffs are only paused, and every country in the world is still subject to a baseline 10%. They could just as easily be turned back on.

Besides, if Trump really wanted to win friends and influence ‘allies’ like Canada he has a peculiar way of showing it: insulting Canada and its leaders and threatening to use economic force to annex the country. Canadians have their ‘elbows up’ and are in no mood to play along with Trump’s schemes.

Had he really wanted to build a bulwark to counter China’s trading practices, as we are now meant to believe, he could have built a coalition from the beginning, while pausing sector-specific tariffs on Canada’s auto sector, which he chose not to do. Investors should remain cautious about Trump’s proclamations and overtures on Truth Social or his ever-shifting plans.

More likely, the disordered approach reflects Trump's long-held (and grossly mistaken) belief that U.S. trade balances should be at a minimum neutral, and ideally in surplus, with every country in the world.

Perhaps the conflicting messages and policies coming from the White House are indeed part of some carefully pre-meditated plan for Trump to appear the “mad man” to get others to the negotiating table to strike a grand bargain on trade. Let’s hope that’s the case. Because

negotiating away both Trump's real and imagined non-tariff barriers with every trading partner will prove next to impossible, in which case get ready for more threats, deadlines and tariff hikes from the "mad king."

|

|

THIS WEEK ON DEFI DECODED

|

|

|

|

|

|

Join Alex Tapscott and Andrew Young as they decode the world of Web3 with special guest James Seyffart, ETF Research Analyst at Bloomberg Intelligence. Listen in as they discuss what’s happened with ETFs amid this past week’s market turmoil, the meaning of terms like ‘bearish but long’ and ‘Vanguard put,’ and how they relate to current investing trends, where most ETF flows are going, ETF trading volumes by asset class, key indicators to watch for gauging market sentiment, whether James sees any signs of market strain from the ETF lens, thoughts on new products that short leveraged ETFs, the influx of crypto ETF filings, whether the SEC will greenlight staking for crypto ETFs, the pros and cons of gaining crypto exposure through public corporation vehicles versus ETFs, the collapse in Grayscale’s Solana Trust premium and what it signals for SOL ETFs, how institutional investors are thinking about Bitcoin, the crypto market outlook for the second half of the year, the recent divergence between Bitcoin and crypto equities, and more.

|

|

|

|

By: Jake Moodie

, Analyst, Digital Asset Group at Ninepoint Partners

SEC Clarifies That Stablecoins are Not a Security, Unless They Pass Yield Through to Holders

The SEC is continuing to follow through on its promise to bring positive regulatory reform to crypto. This week, they released a

statement to clarify their view on stablecoins. In the statement, they said that, in their view, stablecoins are not securities. To be specific, they were referring to USD-backed stablecoins that are fully redeemable one-for-one and backed by reserves that meet or exceed the total value of stablecoins in circulation. That said, the SEC also made it clear that stablecoin issuers can’t pass along interest through to holders, and if they do, that makes it a security. Right now, firms like Tether and Circle keep all the yield from the reserves they invest into government securities. Still, overall, this is a step in the right direction and welcomed by the industry, who has been asking for clarity for a long time. The SEC has also recently clarified that proof-of-work mining doesn’t involve securities—and that the same goes for memecoins.

Ripple Buys Prime Broker Hidden Road for $1.25B, One of the Largest Deals in Crypto History

Ripple has

announced that it’s acquiring prime broker Hidden Road for $1.25 billion, making it one of the biggest M&A deals in crypto history. Hidden Road works with over 300 institutional clients, offering a full range of services including clearing, prime brokerage, and financing across digital assets, fixed income, derivatives, swaps, and foreign exchange. They clear over $3 trillion across markets every year. As part of the deal, Hidden Road will start using Ripple’s RLUSD stablecoin as collateral across its prime brokerage products and move its post-trade activity over to Ripple’s XRP Ledger blockchain. Like we talked about before, crypto M&A season kicked off in November with Stripe’s $1.1 billion acquisition of stablecoin firm Bridge. Since then, MoonPay bought Helio and Iron, Chainalysis picked up Alterya, Kraken acquired NinjaTrader, and Magic Eden acquired Slingshot. There were also rumours that Coinbase was eyeing Deribit. Ripple’s deal still needs regulatory approval, but it’s expected to close by Q3 2025.

|

|

|

|

|

|

|

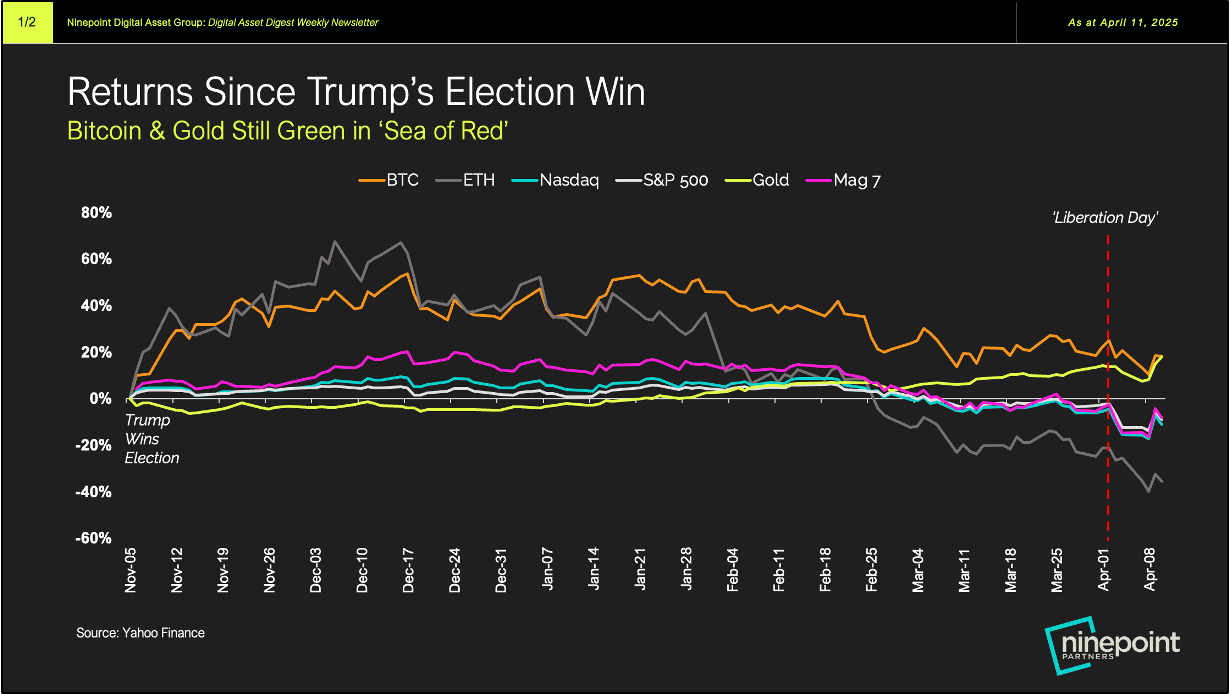

Chart 1: Trump Trade Revisited: Bitcoin and Gold Lead While All Others Lag

|

Cryptoassets like Bitcoin were, for a time, the darlings of the so-called “Trump Trade,” a basket of financial assets expected to benefit from a Trump presidency, surging in the aftermath of the election as Trump pledged to completely overhaul the government’s approach to the industry. While cryptoasset prices have declined alongside broader markets amid recent turmoil, Bitcoin remains up 18% since the election. For perspective, the S&P 500 is down 9%, and the Nasdaq is down 11%. Gold is the only asset class that has positively with Bitcoin, and even after its impressive recent rally, is up the same 18%. To be sure, most cryptoassets haven’t followed Bitcoin’s trajectory. Ethereum is down 36%, and crypto-related public equities have experienced similarly large drawdowns. Questions remain as to whether these equities will benefit from a potential decoupling or be swept up in the continued selloff. As such, we remain cautious.

|

|

|

|

|

|

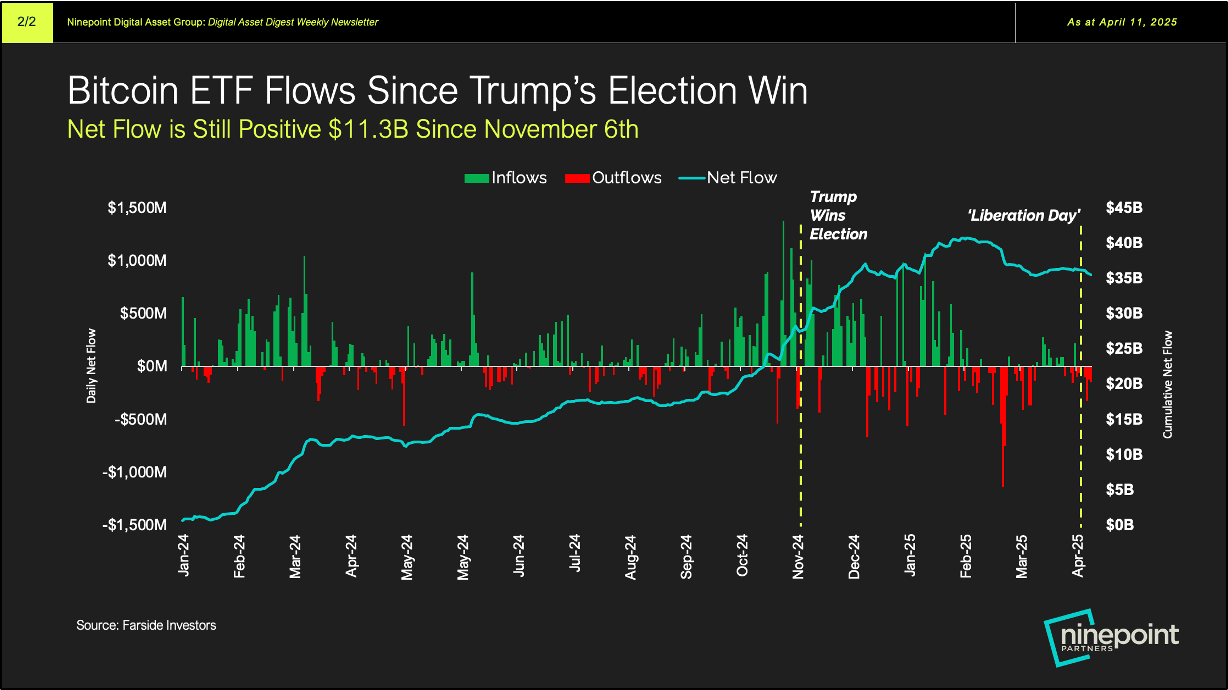

Chart 2: Bitcoin ETFs Have Weathered the Storm with Over $11B in Net Flows Since Trump’s Election Win

|

With Bloomberg Intelligence ETF Research Analyst James Seyffart

joining the DeFi Decoded podcast this week as our special guest, we thought it was the perfect time to discuss the latest on Bitcoin ETF flows. In the 30 days following Trump’s election victory, Bitcoin ETFs

saw net inflows of $15.8 billion, helping propel Bitcoin to a new all-time high of nearly $110,000. Since then, in the past 90 days, these products have experienced a more modest $1.5 billion in net inflows. The most fascinating aspect about this chart is that the launch of the Bitcoin ETFs was the most successful in history by flows, which was an accolade achieved well before the volatility seen on the right-hand side of the chart, both to the upside and downside. Even amid the recent market selloff, Bitcoin ETFs have still accumulated $11.3 billion in net assets since Trump’s election victory. This is probably helping provide some support to Bitcoin’s relatively more stable price compared with other asset classes in recent weeks. To hear more about ETF flows, not just in crypto, but also in TradFi, tune in to this week’s

episode!

|

|

|

April 11, 2025

April 11, 2025