Ninepoint Target Income Fund

Q1 2023 Commentary

The Ninepoint Target Income Fund March 2023 Quarterly Update

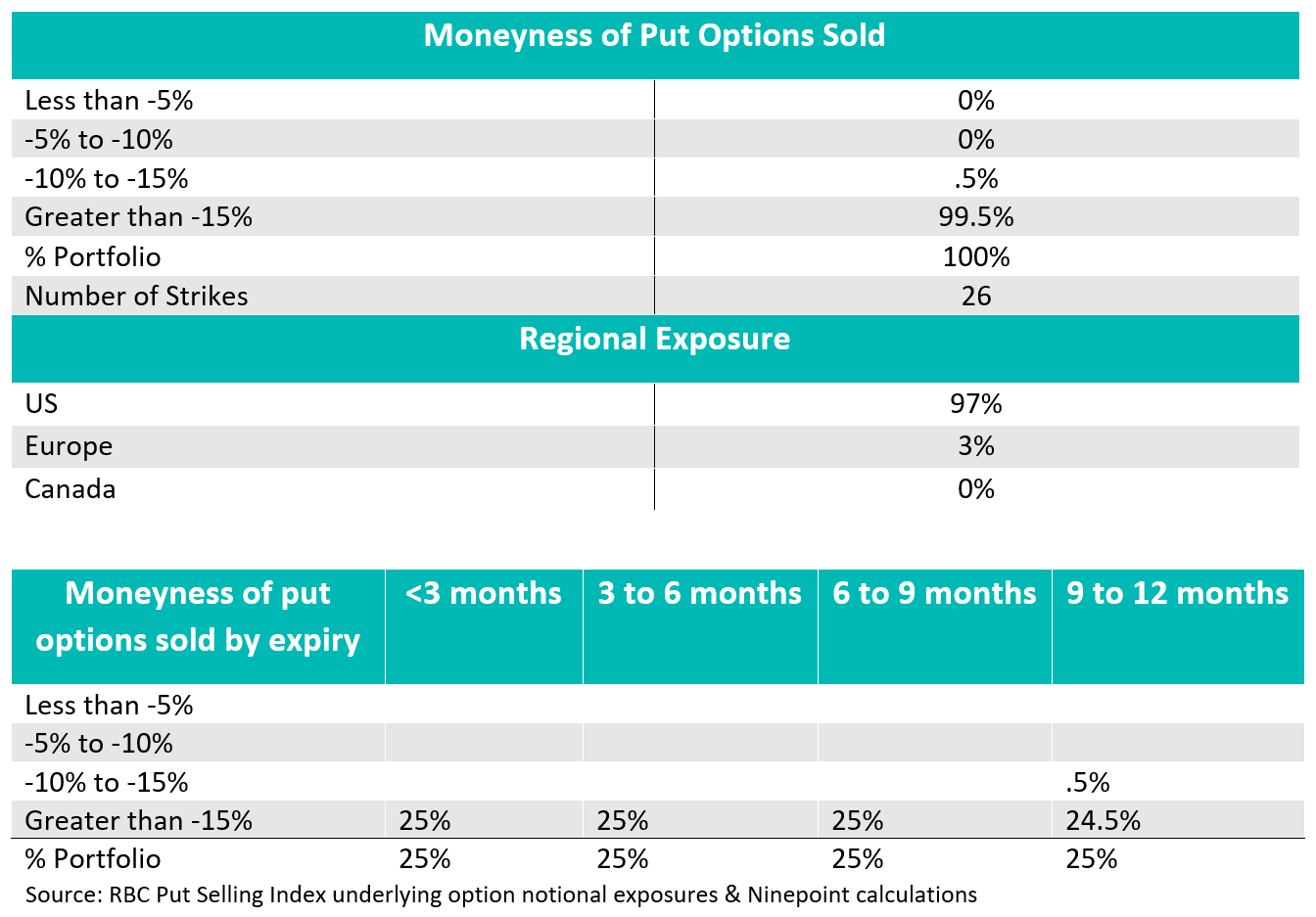

Equity markets ended the quarter with a strong rally and near full retracement of the March declines, as regional bank balance sheet concerns subsided, and large cap technology shares rallied. Regional bank solvency concerns initially drove a spike in equity implied volatility, offering a higher potential yield for newly initiated put options. The Target Income Fund came into March options expiry with a low risk profile and was able to take advantage of elevated put yields when the rules-based approaches rolled into new 1 year put options. This lifted the total potential yield of the option portfolio at that point in time. Nearly all the options have a strike price greater than -15% below March 31st index levels, providing a sizeable buffer before premiums are put at risk.

Technology & growth-related sectors have now contributed nearly all the gains in the S&P 500 so far this year, offsetting the recent weakness in cyclical sectors and leading to an S&P 500 index that on aggregate, is close to the February highs but with increasingly concentrated leadership. While there are some early signs that revenue growth could be troughing for several key tech companies, we view the fall in long term interest rates as the primary driver of the rally in tech which could potentially put the rally at risk if rates were to rise again.

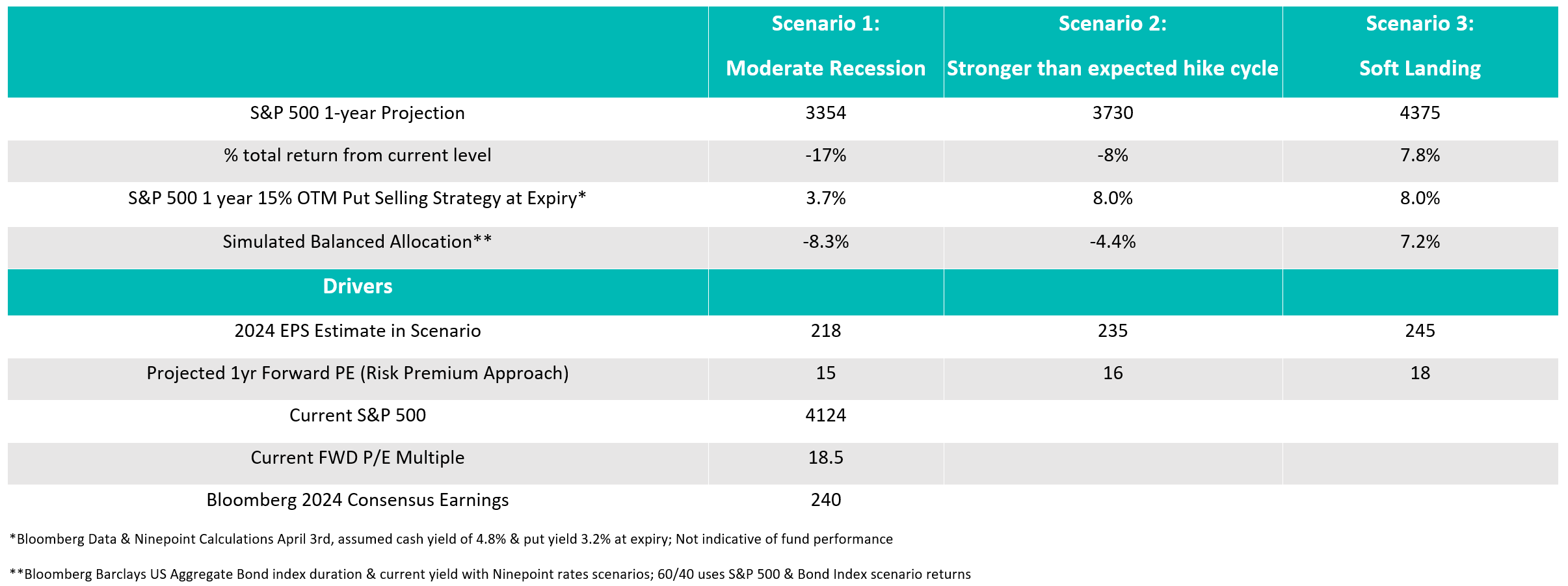

After the most recent gains, equities are for the second time this year, more forcefully pricing in our base case upside scenario of a successful fed pivot and economic soft-landing, which lowers the attractiveness of traditional long only equity exposure in our view. Building on the fundamental scenario analysis we presented in January; we include an example of a potential return at expiry, of a 1-year S&P 500 15% out-the-money put selling strategy compared to a simulated 60/40 portfolio and the S&P 500 standalone. If you agree with these simplified scenarios as the most likely path forward, then owning the put selling strategy has limited upside opportunity cost vs the S&P 500 and balanced allocation, while potentially providing a more defensive portfolio in the more draconian downside scenarios. Despite our view that traditional fixed income allocations will provide better diversification for stocks vs 2022, the cash covered put selling example offers strong risk reward asymmetry.

For illustrative purposes only

For illustrative purposes only

In 2023, equity markets have cycled through repricing some degree of all three of the base case scenarios we outlined in our year ahead commentary. The short-lived equity market correction and sharp rotation back into tech, an underweight sector for many, continues to create a difficult backdrop for both traditional long only equity strategies and more tactical investors seeking a better entry point. We suspect the path ahead continues to offer investors more of the same, a whole lot of volatile price action with limited follow through. If this is correct, it will continue to favour put selling on a risk adjusted basis, as they are uniquely positioned for rangebound environments.

For illustrative purposes only

For illustrative purposes only

Until Next Time,

Colin Watson

Portfolio Manager

Ninepoint Partners

Why Invest in the Ninepoint Target Income Fund?

- Targeted Equity Yield: The Target Income Fund utilizes a cash covered put selling strategy to target a 6% yield while potentially offering a buffer against market declines

- Accessible: Offered in a low-medium risk rated traditional mutual fund structure with daily liquidity at NAV

- Income Potential & Diversification: options-based income strategies can offer a competitive yield and may provide diversification to traditional income portfolios during challenging markets

- Execution Partnership: Leverages RBC Quantitative Investment Solutions diversified, rules based put selling strategies to generate income and diversification

Ninepoint Partners LP is the investment manager to the Ninepoint Funds (collectively, the “Funds”). Important information about the Ninepoint Partners LP Funds, including their investment objectives and strategies, purchase options, and applicable management fees, performance fees (if any), other charges and expenses, is contained in their respective simplified prospectus, long-form prospectus or offering memorandum. Please read these documents carefully before investing. Commissions, trailing commissions, management fees, performance fees, other charges and expenses all may be associated with investing in the Ninepoint Partners LP Funds. Unless noted otherwise, the indicated rates of return for one or more classes or series of units or shares of the Ninepoint Partners LP Funds for periods greater than one year are based on historical annual compounded total returns and include changes in unit/share value and reinvestment of all distributions or dividends, but do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Ninepoint Partners LP Funds referred to on this website may be lawfully sold in their jurisdiction.

The Ninepoint Target Income Fund is generally exposed to the following risks. See the simplified prospectus of the Fund for a description of these risks: Absence of an active market for ETF Series risk; Concentration risk; Currency risk; Derivatives risk; Foreign investment risk; Halted trading of ETF Series risk; Inflation risk; Interest rate risk; Liquidity risk; Market risk; Securities lending, repurchase and reverse repurchase transactions risk; Series risk; Short selling risk; Substantial unitholder risk; Tax risk and Trading price of ETF Series risk.

Ninepoint Partners LP: Toll Free: 1.866.299.9906. DEALER SERVICES: CIBC Mellon GSSC Record Keeping Services: Toll Free: 1.877.358.0540

Related Funds

Toronto, Ontario M5J 2J1 Canada