Ninepoint Carbon Credit ETF Commentary

April 2023 Commentary

Fund Overview

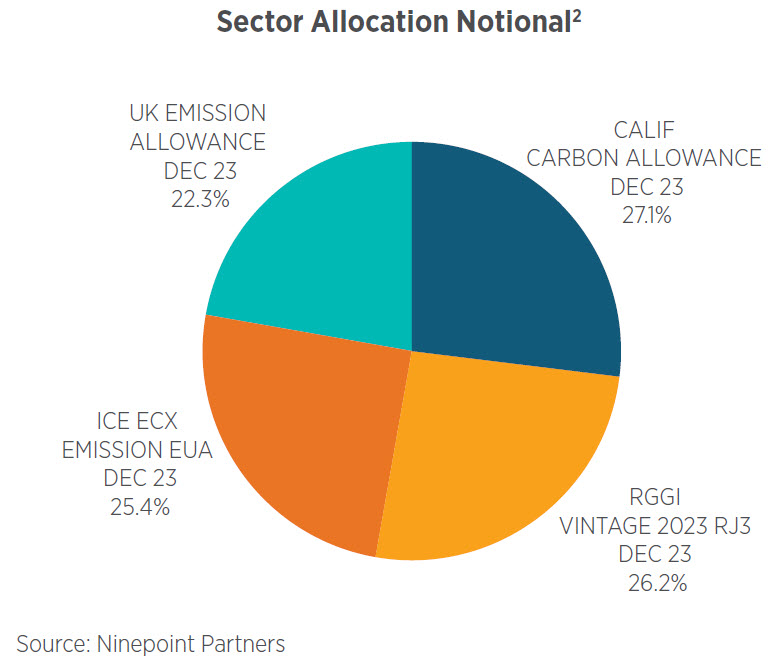

The Ninepoint Carbon Credit ETF (“Fund”) seeks to achieve its investment objectives by primarily investing directly in carbon allowance futures. The Fund currently invests in the major carbon allowance futures globally, namely;

- European Union Allowance (the “EUA”)

- California Carbon Allowance (the “CCA”)

- UK Allowance (the “UKA”)

- Regional Greenhouse Gas Initiative (the “RGGI”)

Fund Performance

As of April 30, 2023, the Ninepoint Carbon Credit ETF generated a return of -5.10% (Series F $USD), with a net year-to-date net return of -3.22%.

Market Update

Breaking developments from late April: First Republic Bank became the second biggest bank failure in the US history on May 1st, after the bank revealed in its earnings report of April 24th that it had experienced deposit withdrawals of more than $100 billion in the wake of the SVB collapse in March, which made the continuation of the California-based institution untenable. It was consequently taken over by the FDIC after shares of the bank had lost 97% at market close on April 28th, and its assets were sold to JP Morgan Chase. The beginning of 2023 has certainly been eventful for the US banking sector, with three of the largest FDIC failures of the century occurring within the span of a few weeks.

Fears of a potential recession later this year were bolstered by U.S. GDP growing at just a 1.1% annualized pace in the first quarter, as well as very gradual hints of slowing in the tight labor market. However, within equity alternatives, commodities experienced a positive month as industrial metals (notably copper) reached new highs driven by both supply shortages and structural demand for technology and alternative energy manufacturers.

The end of the month concluded with the S&P 500 up 1.56% (9.16% YTD), the Bloomberg Commodity Index down -1.13% (-8.21% YTD), Brent Oil down -0.44% (-9.86% YTD), and Gold up 0.14% (11.93% YTD).

Financial markets were increasingly concerned about the debt limit and the lack of meaningful progress in extending it. On the other hand, the majority of 2023 global growth is predicted to come from Asia, with China’s economic growth expected to be at around 6%, as a result of the complete abandonment of pandemic control policies which prompted nationwide mobility and robust economic activity.

Portfolio Update

In the carbon market, the month of April was quite gloomy, especially across the pond. The European Union Allowance (EUA) Dec-23 contract was down -5%. The market seems isolated from political and regulatory risks now that market reforms and REPowerEU packages have been approved, which are also expected to bring additional supply to the market by front loading auction sales slated for later years to fund the pivot away from Russian fossil fuels. That said, the market continued to trade lower through the month of April as buying support from emitters dropped-off ahead of the April 30 compliance deadline and since overall demand in the European Union dropped in 2022 after factories curbed production as a result of soaring costs due to the energy crisis. The UK Allowance (UKA) Dec-23 contract also declined by -17.17%. The market seems to be currently flooded with excess supply amid annual verified emissions that are regularly below the cap, with no mechanism in place to deal with this other than the government withholding free allocations and limiting auction volumes.

In North America, the ICE California Carbon Allowance (CCA) Carbon Futures Index gained 3.25% this month. The slow but steady move higher over the past weeks was in part driven by a continued supportive macro environment, increases in both compliance buying and investor interest, as well as continued strength for Washington Carbon Allowance. The ICE Regional Greenhouse Gas Initiative (RGGI) Carbon Futures Index posted a loss of 1.27% this month, despite the Program Review taking place at the end of March. The market is likely to remain range bound in the near-term as we enter the spring months and the typical decreased demand for power generation.

Portfolio Recap

The fund has had a challenging start to the year, posting a net loss of 3.22% year-to-date. The best performer in April was the CCA market, contributing approximately +0.79% to the total return, the top distractor was the UKA contract, contributing approximately -4.31% to the total return.

Why Ninepoint Carbon Credit ETF?

For an emerging asset class like carbon credit, diversification is at the heart of our fund strategy. At the moment, the Ninepoint Carbon Credit ETF invests equally in the four major ETS markets globally with a minimum quarterly rebalancing. Having a diverse market exposure has demonstrated its benefits in serving investors well. Below are five key reasons for investors to consider Ninepoint Carbon Credit ETF:

Risk Mitigation – Balanced exposure to all carbon credit markets can help minimize single jurisdiction risk by eliminating over-concentration to any single market, as recent market action has demonstrated. Having a diversified underlying market portfolio is important for an emerging asset class with volatile price patterns, like carbon credits.

Diversification – Carbon Credit investments demonstrate low or negative correlation to traditional asset classes.

Global Exposure – The fund provides investors with access to a US$851 billion global carbon credit market which has grown by 18x since 20171. Compared to volume-weighted fund or funds that invest in one single market, we believe that our equal-weighted fund strategy has a better value proposition, over the long-term, given its overweight to the under-represented and rapidly growing carbon credit trading markets.

Core Value - As a Canadian fund, by overweighting the North American market relative to its total index weight, we are aligning our strategy with our values and our local community.

Easy Access - The fund is structured as an alternative mutual fund offering on Fundserv as well as an ETF series on the Cboe Canada Exchange (Cboe:CBON / CBON.U).

Product Inquiries:

Pamela Gagne, MBA

Business Development Manager

Ninepoint Partners

pgagne@ninepoint.com

1Refinitiv, “Carbon Market Year in Review 2021”.

Global carbon markets value surged to a record $851 bln last year-Refinitiv (Reuters - January 2022).

1All returns and fund details are a) based on Series F $USD units; b) net of fees; c) annualized if period is greater than one year; d) as at April 30, 2023.

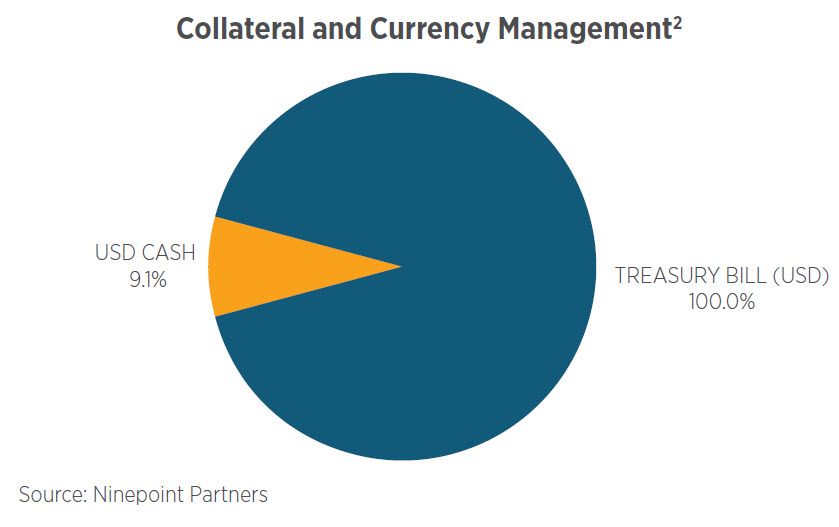

2Sector allocation as at April 30, 2023. Sector allocation based on % of net asset value. Numbers may not add up due to rounding. Cash and cash equivalents include non-portfolio assets and/or liabilities.

The Ninepoint Carbon Credit ETF is generally exposed to the following risks See the prospectus of the Fund for a description of these risks Absence of an active market for ETF Series risk, cap and trade risk, collateral risk, commodity risk, concentration risk, cybersecurity risk, derivatives risk, foreign currency risk, foreign investment risk, Halted trading of ETF Series risk, inflation risk, interest rate risk, liquidity risk, market risk, regulatory risk, securities lending, repurchase and reverse repurchase transactions risk, series risk, substantial securityholder risk, tax risk, trading price of etf series risk.

Ninepoint Partners LP is the investment manager to the Ninepoint Funds (collectively, the “Funds”). Commissions, trailing commissions, management fees, performance fees (if any), and other expenses all may be associated with investing in the Funds. Please read the prospectus carefully before investing. The indicated rate of return for series F shares of the Fund for the period ended April 30, 2023 is based on the historical annual compounded total return including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Fund may be lawfully sold in their jurisdiction.

The opinions, estimates and projections (“information”) contained within this report are solely those of Ninepoint Partners LP and are subject to change without notice. Ninepoint Partners makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Ninepoint Partners assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Ninepoint Partners is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Ninepoint Partners. Any reference to a particular company is for illustrative purposes only and should not to be considered as investment advice or a recommendation to buy or sell nor should it be considered as an indication of how the portfolio of any investment fund managed by Ninepoint Partners is or will be invested. Ninepoint Partners LP and/or its affiliates may collectively beneficially own/control 1% or more of any class of the equity securities of the issuers mentioned in this report. Ninepoint Partners LP and/or its affiliates may hold short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, Ninepoint Partners LP and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

Ninepoint Partners LP: Toll Free: 1.866.299.9906. DEALER SERVICES: CIBC Mellon GSSC Record Keeping Services: Toll Free: 1.877.358.0540

Investment Team

Related Funds

Toronto, Ontario M5J 2J1 Canada