Ninepoint Alternative Health Fund

September 2023 Commentary

Summary

September saw continued interest in the US cannabis sector on the heels of announcements from Washington. Both the Aug 29th announcements, HHS recommending that cannabis be re-scheduled to Schedule III on the Controlled Substances Act and then the subsequent US Senate announcement bringing the SAFER Banking Act to the floor, are all that added renewed enthusiasm and momentum to the sector. There is still volatility in this nascent industry, where government regulation prevents markets from fully being established, however, indications suggest regulatory changes towards efficient and open markets in the US are on the horizon. US cannabis companies using their strong cash positions with companies such as TRUL repurchasing $57 million of the $425 million in notes due in 2026 for only $47.6 million (a 16.5% discount) and in the case of GTI, pursuant to a normal course issuer bid, announced a share purchase plan for up to $50 million of its Subordinate Voting Shares over the next 12-month period. The other major catalyst the fund has been analyzing is the development of breakthrough treatments dealing with type II diabetes and obesity medications. Pharmaceutical companies such as NOVO and LLY are the early leaders in this developing global market.

September Update

For the month, the Fund had strong performance from its leading US cannabis positions including GTI, TRUL, and VRNO as well as from COST and UNH.

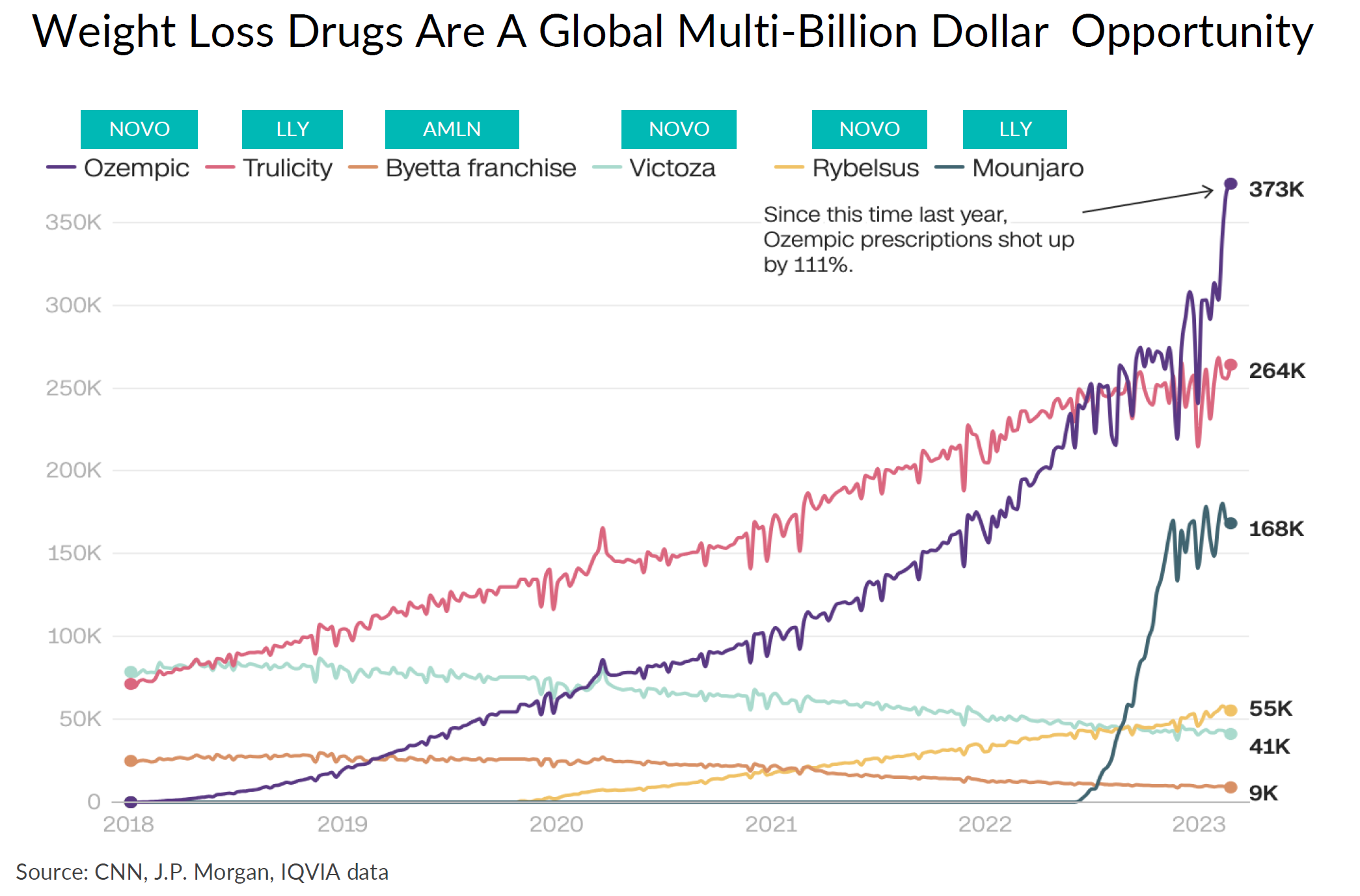

Update on Breakthrough GLP-1 Drugs: Ozempic, Rebellsys…

Decades of stigma and discrimination toward people who display higher BMI (+30 BMI results in categorization as obese) in North America are pervasive and pose challenges for healthcare solutions on both a physical and psychological basis. It is estimated that 40% of American adults have a BMI of +30, and research shows that a high BMI can lead to many co-morbidities that have significant healthcare cost implications. This is one of the key reasons the breakthrough drugs, known as the GLP-1 drugs, see so much attention related to the potential for government-funded healthcare programs. GLP-1 drugs have been considered “vanity drugs” because they provide accelerated weight loss benefits, however, the recent phase II study that illustrated a marked 20% drop in MACE (major adverse cardiac events), provides more insight into the long-term benefit for healthcare funding as so many related co-morbidities will be reduced over time. Current revenue from these GLP-1 drugs is estimated at $22 billion globally, with forecasts from BMO and Jefferies to reach $55 to $70 billion over the next decade. Key to the growth anticipated is to get cooperation amongst politicians, regulators, and physicians to understand the long-term health benefits, balanced with the recognized upfront costs of covering these drugs vs the long-term efficiencies for the health care system. The Fund owns Eli Lilly (LLY), one of the leaders in the GLP-1 space.

US Re-Scheduling Cannabis Update: Next Steps

On Aug. 29, the Department of Health and Human Services (HHS) responded to President Joe Biden’s call last October for a review of marijuana scheduling under federal law. The HHS decision was that cannabis should be reclassified as a Schedule III drug. Please see our previous commentaries for background and implications on the positive cash flow implications for multi-state operators.

The decision from HHS is significant as it is the first official US government acknowledgment that marijuana has medicinal value. Its previous stance was that because cannabis had no medicinal value, and tended to be a gateway drug was the primary reasoning behind its Schedule I classification. With HHS medical data, it is over to the DEA. DEA Administrator Anne Milgram, a 2021 Biden appointee, along with federal attorneys will consider relevant questions of law and policy, however they cannot overrule HHS medical findings. We believe that in addition to the DEA re-scheduling confirmation, we see Attorney General Marrick Garland providing a “Cole Memo” type of Department of Justice directive to further reduce the business risk associated with cannabis, while still staying federally illegal. This memo along with the re-scheduling to III would result in a very different and positive landscape for the cannabis industry. We could say as a result that, cannabis’ days as a Schedule 1 drug are ending.

There is recent precedence to adjust cannabis to Schedule III. The drug Epidiolex, at the time developed by GW Pharma, is a THC-based medication that has been proven to assist in controlling epileptic seizures and became a Schedule III drug in 2018. Further supporting a positive outcome on re-scheduling was a report from the Congressional Research Service that suggests the DEA is likely to follow the recent HHS recommendation to re-schedule cannabis from Schedule I to Schedule III, with the CRS being unaware of an instance where the DEA has rejected medical claims from HHS. Timing is uncertain for the DEA to make its decision, however, it is our belief that the DEA will make its announcement over the next 3 to 6 months.

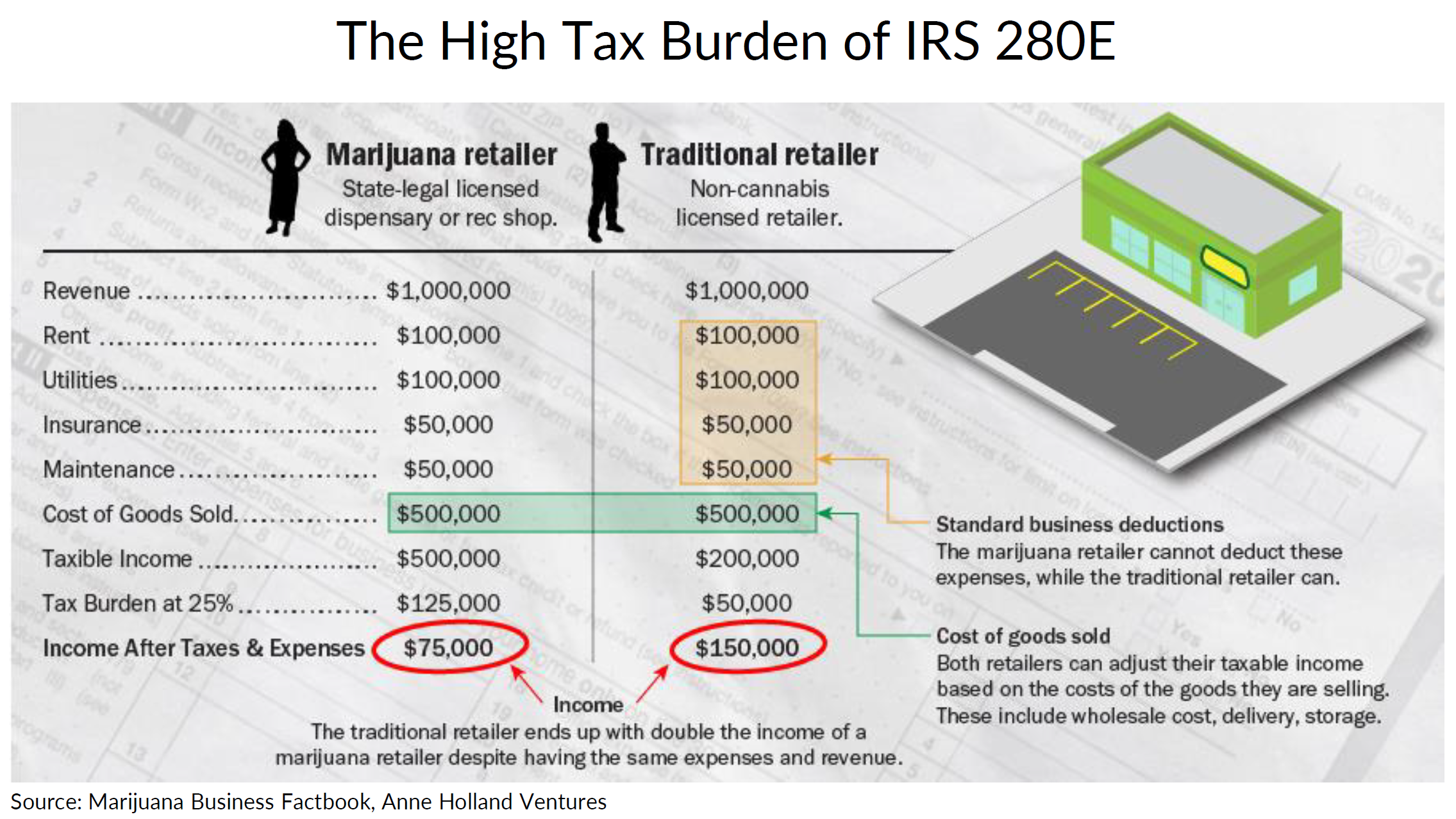

Why do we emphasize the details of Schedule III and what are the implications for US cannabis stocks? As we stated last month, rescheduling to Schedule III leads to the removal of IRS Code 280E, an onerous tax regime. A company that produces a Schedule I drug operates under Section 280E of the Internal Revenue Code, which states businesses are prohibited from taking normal business deductions such as salaries, rent, and interest expenses when calculating tax liabilities. It means that MSOs are in effect paying tax on gross profit, resulting in effective tax rates of 50-70%+, rather than other businesses with regular deductions that bring their effective tax rates to 21%, meaningfully improving the cash flow profile of the sector. This is the reason behind cannabis stocks rallying since Aug 29. We believe that when the DEA comes out with its report, we anticipate significant further upside in US cannabis names which will lead to further federal legislative changes allowing the cannabis market to grow.

Ohio Ballot Initiative: The 24th State

On November 7, another major US state market could transition from medical to recreational. Ohio is holding a ballot initiative where momentum and support are strong to legalize adult-use cannabis. The vote if successful, would be the third state this year to transition, after Delaware and Minnesota, both of which took the legislative route to legalize marijuana. Ohio would be the 24th legal market in the US, allowing for cultivation, production and sales of adult-use cannabis. OH, is important not just because it is another market. OH, holds strategic value as it is another top ten state in terms of population with over ten million residents representing a large potential recreational market. It is also important as OH is seen as a Republican-dominated state and bringing a “Red” state into the cannabis market is noteworthy as it results in two additional Republicans in the US Senate that could see the job growth and state tax generation of this industry. Ohio is also important as it is a limited license state, with a positive vote resulting in the issuance of 40 Rec cultivator licenses and fifty adult-use retail licenses, with more licenses to be issued in future. Ohio will join a growing list of midwestern states like Illinois, Michigan, Missouri (and Minnesota already mentioned) that have approved possession and retail sales of adult-use cannabis that could create more pressure on the federal government to move forward with measures like Re-scheduling and federal banking legislative changes to enhance industry functioning. A recent survey conducted by Fallon Research found that most of the Ohioans support legalization with 59% in favor, 32% opposed, and 9% undecided at that time.

The Fund offers leverage to this growing market with positions in Ohio incumbent MSOs such as Green Thumb Industries (GTI), Verano Holdings (VRNO), Trulieve Cannabis (TRUL), Cresco Labs (CL), with a head start in the market that represents $1 billion+ in annual sales in the near term.

SAFER Banking Act: Senate Takes a Step Forward

The SAFER Banking Act (SAFE) to provide better access to financial services for MRBs had its first positive committee vote on September 27 in the Senate Banking Committee. SAFER is a revised version of the SAFE Banking Act that passed the House seven times in the past ten years, but to date has failed to gain ground in the Senate. Revisions to SAFE that resulted in SAFER include protections from federal interference for banking services with guidance to be provided by the FDIC, qualification for mortgages, collaboration with state regulators, and additional emphasis on social equity reforms. The passage of SAFER as currently drafted would allow credit cards to be used in dispensaries, which has the potential to increase sales by approx. 20% since electronic payments have higher average ticket sizes than cash. Currently, dispensaries only have a 10% penetration of electronic payments vs 70% for all other retailers so allowing credit card transactions could represent a significant growth catalyst for MSOs under the new SAFER regime.

SAFER passing in a Senate Committee vote is a good step forward bringing awareness to the longer-term goal of cannabis reform at the federal level and ultimately full legalization. The reason it is noteworthy is that it is the first time in US history that there has been a positive vote on cannabis in the US Senate.

Next step forward is the full Senate vote on the legislation over the next month or two. Potential amendments that could see their way to the legislation are centered on expungement provisions and gun rights for medical cannabis patients. There are also issues to be ironed out with respect to whether legislation will include directives from the federal government that force banks to serve cannabis MRB clients that a bank may perceive as posing “reputational risk.” Some Senators see this language as an overreach of federal authority potentially allowing regulators to block banks from servicing other industry clients where political issues exist such as the energy industry. There will be interesting negotiations in the coming months.

Once the Senate has voted (in favour) of the legislation, it then goes to the House of Representatives. At the current time, the House of Representatives is controlled by the Republicans and given the polarized nature of Washington, we believe there is an uphill battle to get the House to bring SAFER to the floor of the House for a vote, let alone allocate time for committee hearings.

Option Strategy

Since the inception of the option writing program in September 2018, the Fund has generated significant income from options premiums of approximately $4.86 million. We will continue to utilize our options program to look for attractive opportunities given the above-average volatility in the sector as we strongly believe that option writing can continue to add incremental value going forward.

During the month we used our options strategy to assist in rebalancing the portfolio in favor of names we prefer while generating approximately $14,000 in options income. We continue to write covered calls on names we feel are range bound near term and from which we could receive above average premiums which included Tilray Brands Inc. (TLRY) and Cronos Group Inc. (CRON). We also continue to write cash-secured puts out of the money at strike prices that offered opportunities to increase our exposure, at more attractive prices, to names already in the Fund including UnitedHealth Group Inc. (UNH) and Eli Lilly and Co (LLY).

The Ninepoint Alternative Health Fund, launched in March of 2017 is Canada’s first actively managed mutual fund with a focus on the cannabis sector and remains open to new investors, available for purchase daily.

Charles Taerk & Douglas Waterson

The Portfolio Team

Faircourt Asset Management

Sub-Advisor to the Ninepoint Alternative Health Fund

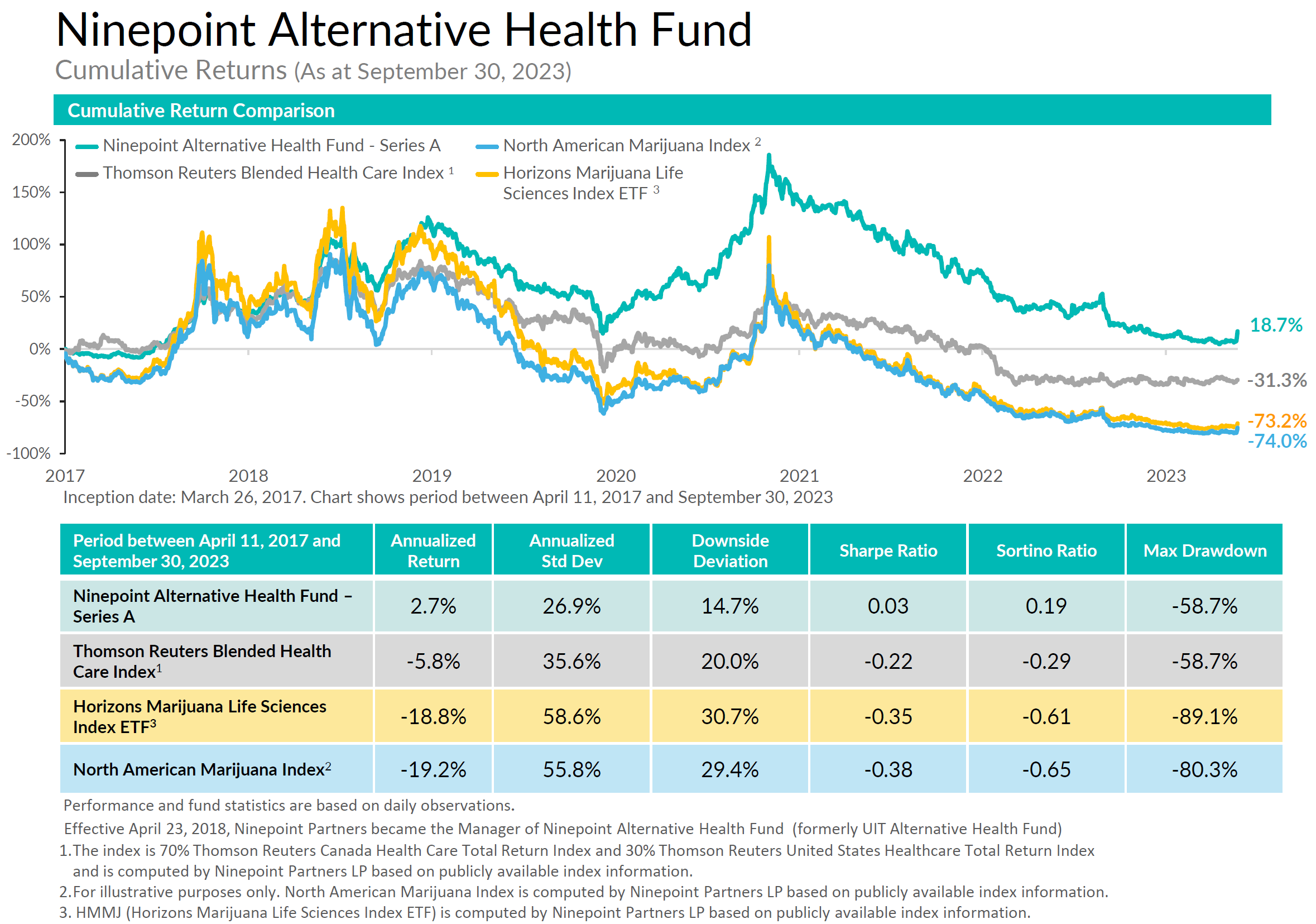

Ninepoint Alternative Health Fund - Compounded Returns¹ as of September 30, 2023 (Series F NPP5421) | Inception Date - August 8, 2017

| MTD | YTD | 3MTH | 6MTH | 1YR | 3YR | 5YR | INCEPTION (ANNUALIZED) |

|

|---|---|---|---|---|---|---|---|---|

| FUND | 1.5% | -3.4% | 9.4% | 5.9% | -8.3% | -8.7% | -9.1% | 4.7% |

| TR CAN/US HEALTH CARE BLENDED INDEX | -2.5% | 4.8% | -0.5% | 1.1% | 0.8% | -9.9% | -17.6% | -6.6% |

Statistical Analysis

| FUND | TR CAN/US HEALTH CARE BLENDED INDEX | |

|---|---|---|

| Cumulative Returns | 32.9% | -34.1% |

| Standard Deviation | 27.3% | 28.9% |

| Sharpe Ratio | 0.1 | -0.3 |

1 All returns and fund details are a) based on Series F units; b) net of fees; c) annualized if period is greater than one year; d) as at September 30, 2023. The index is 70% Thomson Reuters Canada Health Care Total Return Index and 30% Thomson Reuters United States Healthcare Total Return Index and is computed by Ninepoint Partners LP based on publicly available index information.

The Fund is generally exposed to the following risks. See the prospectus of the Fund for a description of these risks: Cannabis sector risk; Concentration risk; Currency risk; Cybersecurity risk; Derivatives risk; Exchange traded fund risk; Foreign investment risk; Inflation risk; Market risk; Regulatory risk; Securities lending, repurchase and reverse repurchase transactions risk; Series risk; Specific issuer risk; Sub-adviser risk; Tax risk.

Ninepoint Partners LP is the investment manager to the Ninepoint Funds (collectively, the “Funds”). Commissions, trailing commissions, management fees, performance fees (if any), and other expenses all may be associated with investing in the Funds. Please read the prospectus carefully before investing. The indicated rate of return for series F shares of the Fund for the period ended September 30, 2023 is based on the historical annual compounded total return including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Fund may be lawfully sold in their jurisdiction.

The opinions, estimates and projections (“information”) contained within this report are solely those of Ninepoint Partners LP and are subject to change without notice. Ninepoint Partners makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Ninepoint Partners assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Ninepoint Partners is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Ninepoint Partners. Any reference to a particular company is for illustrative purposes only and should not to be considered as investment advice or a recommendation to buy or sell nor should it be considered as an indication of how the portfolio of any investment fund managed by Ninepoint Partners is or will be invested. Ninepoint Partners LP and/or its affiliates may collectively beneficially own/control 1% or more of any class of the equity securities of the issuers mentioned in this report. Ninepoint Partners LP and/or its affiliates may hold short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, Ninepoint Partners LP and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

Ninepoint Partners LP: Toll Free: 1.866.299.9906. DEALER SERVICES: CIBC Mellon GSSC Record Keeping Services: Toll Free: 1.877.358.0540

Investment Team

Related Funds

Historical Commentary

- Alternative Health Fund 12/2023

- Alternative Health Fund 11/2023

- Alternative Health Fund 10/2023

- Alternative Health Fund 08/2023

- Alternative Health Fund 07/2023

- Alternative Health Fund 06/2023

- Alternative Health Fund 05/2023

- Alternative Health Fund 04/2023

- Alternative Health Fund 03/2023

- Alternative Health Fund 02/2023

- Alternative Health Fund 01/2023

Toronto, Ontario M5J 2J1 Canada