Ninepoint Alternative Health Fund

December 2023 Commentary

Year End Commentary

The Ninepoint Alternative Health Fund is an actively managed fund whose primary focus is the global cannabis market. To supplement that focus, the fund provides exposure to other innovative and high growth sectors and companies in healthcare, pharmaceuticals as well as health and wellness. In this report, we provide our synopsis of 2023 in addition to our outlook for 2024.

In the year ahead we believe there are several key drivers of growth for the primary sectors within the Fund. We believe that the US cannabis sector has several significant catalysts in its near-term growth trajectory that will benefit investors. Those catalysts include Re-Scheduling Cannabis at the federal level reducing the stigmas attached to the sector and all marijuana related businesses; Changing the punitive IRS 280E tax code affecting cannabis companies thereby re-allocating significant cash flows back to US cannabis operators; State level adult use cannabis transition in Ohio, leading to adult use legislative changes in Pennsylvania; finally, the Ballot Initiative in Florida to bring in Adult Use laws. These three states have large population bases that will drive growth for those that operate in these markets.

We continue to see significant growth for the innovative GLP-1 drugs that are treating obesity and type II diabetes and believe that the companies leading this innovation will continue to see growth in equity value in 2024. Our view is that GLP-1 drugs have the same effect on pharma stocks as AI has had on large cap tech stocks. In addition to these noted growth drivers, we also outline the disruptors providing better access to health services and those companies that are continuing to dominate components of the health and wellness space.

2023 Synopsis

2023 was a year of transition for the Fund as the global economy faced headwinds from inflation risks and higher interest rates that slowed consumer spending and reduced corporate margins. Despite the changes in the economy, the fund maintained several positions that contributed strong annual returns such as Eli Lilly & Co (LLY) +61% in pharmaceuticals; COSTCO (COST) +54% in mass retail; Verano Holdings (VRNO) +40%, Terrasend (TSND) +44% and Green Thumb Industries (GTI) +31% in US cannabis. The sectors at the core of the Fund were challenged in 2023. The core of the fund is in US Cannabis and that sector underperformed for two-thirds of the year. It wasn’t until August when federal re-scheduling of cannabis became a serious catalyst that investor sentiment sector-wide changed for the positive. Pharma excluding LLY & NOVO didn’t have a solid year as the world began to embrace innovations in obesity and type II diabetes treatments at the expense of all other medical breakthroughs.

US Cannabis in 2023

2023 was a challenging year for US cannabis as the sector dealt with a confluence of issues. The US economy witnessed significant inflationary headwinds, backing up into consumer discretionary purchases. Consumer demand was strongly seen in the growth of units sold, however, pricing pressure in states such as Florida, Pennsylvania and Illinois worked to offset volume growth. US Federal legislative reform was elusive in 2023 as Congress continued its dysfunctional path, with extreme right vs extreme left interests grinding most bills to a watered-down consensus, accomplishing very little. Cannabis reform was no different in that broad consensus in Congress remains out of reach despite +60% support nation-wide. Investor sentiment was subdued after nearly two years of waiting for regulatory reform at the federal level, with many investors reaching despondency levels with a perceived futility to wait for substantive federal reform. Despite the macro pressures, the leading multi-state operators (MSO’s) in the Fund continue to generate significant cash flows from operations.

However, we see a significant positive sign of change as the White House has essentially bypassed Congress with its bid to re-schedule Cannabis in the Controlled Substances Act (CSA) to begin the reform process. In our opinion, this change is a major catalyst that will drive 2024.

Investor sentiment has improved substantially since late August when the Department of Health & Human Services (HHS) announced its recommendation to re-schedule cannabis to Schedule III, supporting President Biden’s October 6, 2022 announcement to review the Controlled Substances Act (CSA). Since August, and into the new year, re-scheduling has re-ignited the sector with anticipation of the next positive steps to take place early in 2024.

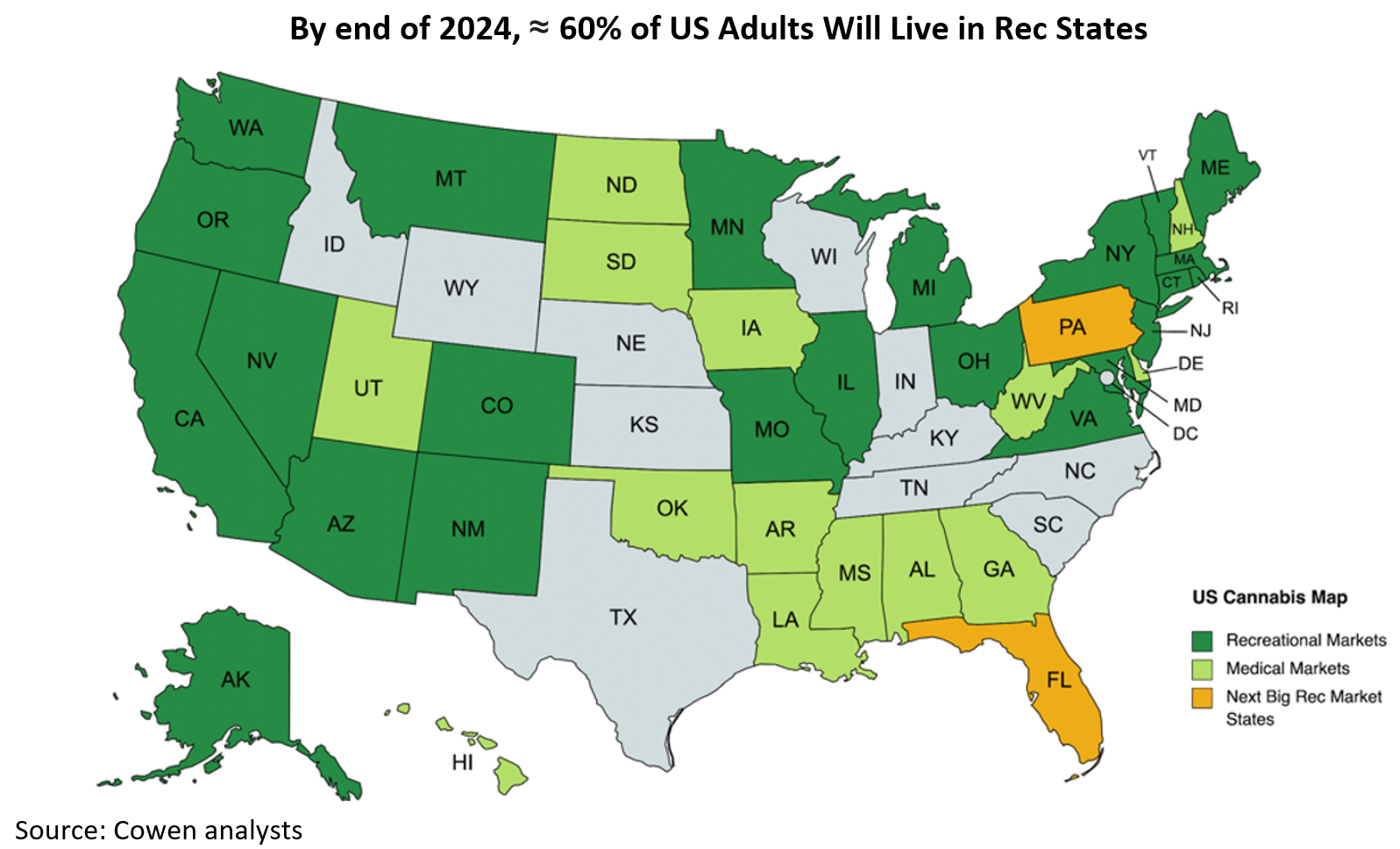

US state recreational markets reached 24 (plus D.C.) as the state legislatures in Delaware and Minnesota brought changes to their laws in April and May, while Ohio transitioned to recreational status through a ballot initiative in November. With Ohio, the 7th most populous state at 12 million, the US now has a majority of its population living in a cannabis-legal state market.

2023 Pharmaceuticals Synopsis: GLP-1 Breakthroughs

2023 was a year for new breakthroughs in the treatment of weight loss and type two diabetes with companies involved seeing significant growth in demand for treatment concurrent with significant growth in stock performance. With positive clinical trials for household prescription names such as Ozempic and Rybelsus, this sector was on fire in 2023. The year was marked by increased awareness on the effectiveness of weight loss and related health concerns that combined to drive demand. That demand, despite the cost of medication and lack of US government insurance coverage saw supply shortages regularly making headlines. Further growth in the GLP-1s was enhanced by data that showed improvements in secondary endpoints or the long-term health complications related to obesity. These trial results have put the GLP-1s on a strong trajectory into the next decade in terms of medical practitioner awareness, patient willingness and private insurance acceptance.

2024 Outlook

US Cannabis: A Positive Year Ahead

Federal Push to Re-Schedule

The biggest near-term catalyst facing the cannabis sector is the potential rescheduling of cannabis by the Biden Administration, currently being reviewed by the Drug Enforcement Administration (DEA). This change represents a significant opportunity for the industry as it potentially opens the door to reduced regulatory burden, broader acceptance, and expanded consumer access in addition to enhanced integration into the mainstream of consumer choice. Looking at the big picture, the executive branch of the US government (the Biden White House) is in the process of easing its policies on marijuana for the first time in 50 years. It does not matter the timing of the decision, it could be Jan 10 or March 22, what matters is that this process is happening. The result is positive for the sector.

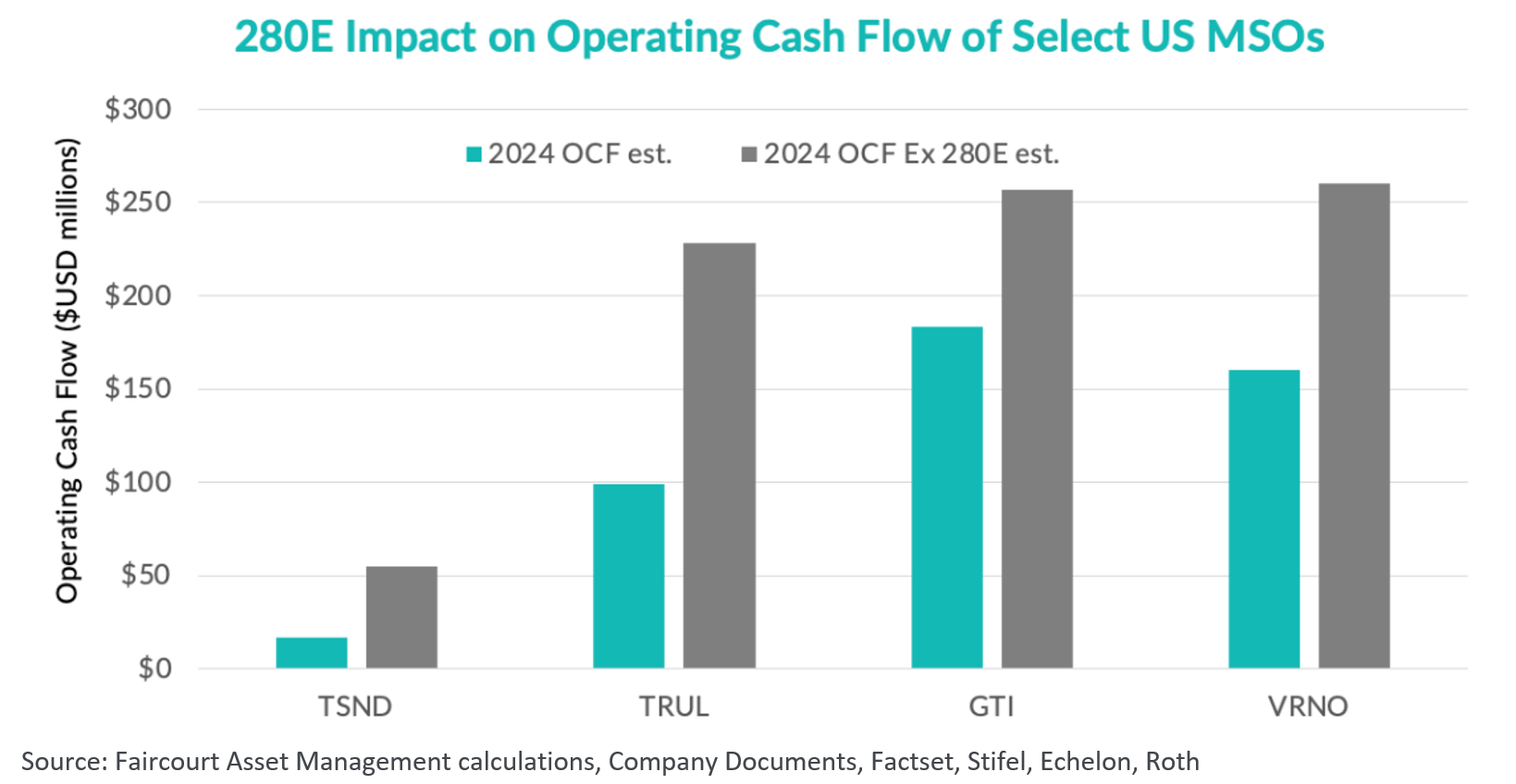

There are numerous benefits to re-scheduling cannabis from Schedule I to Schedule III. Moving to Schedule III would remove the application of IRS tax code provision 280E, which precludes cannabis companies from taking tax deductions available to normal businesses. This would significantly reduce the tax rates and increase the operating cash flow of all multi-state operators. The effect varies for each company based on the amount of cultivation, processing and distribution the company provides in addition to the number of storefronts, among other factors, to determine the extent of benefits from reduced taxation. Regardless, the important point is that the cash flow benefit is significant for every company in the US cannabis space should 280E be repealed. We believe that as an extension of that enhanced cash flow, EBITDA multiples should also move higher as there will be additional resources upon which US cannabis companies can grow. Reviewing the August-September period when Health & Human Services (HHS) came out with its Schedule III medical and scientific review, the largest MSO average EBITDA multiples went from 6.1x to surpass 9.5x, on the prospect of the repeal of 280E. When we compare cannabis to other regulated consumer discretionary sectors such as alcohol which trades at 16x EBITDA or tobacco trades at 12x PE, we believe there is significant upside from these regulatory developments that are a matter of when, not if.

Re-Scheduling & State Level Trigger Laws

As a result of changes to the Controlled Substances Act (CSA) at the federal level, various US states have constitutional rules that would either automatically reschedule medical marijuana to be consistent with the new federal law or at a minimum would begin a process to reclassify cannabis. These changes could be impacted by politics and can have a significant influence on state-level criminal justice reforms not to mention adjusting state-level marijuana programs.

These rules are commonly known as “trigger laws” that essentially result in a state adopting a new federal law automatically. In this case, many states would automatically trigger state-level rescheduling. In Texas where cannabis is confined to limited medical ailments and low dosage THC only, trigger laws could result in medical cannabis becoming more broadly available with more ailments covered in addition to higher THC caps. In states where cannabis is currently illegal, such as Idaho, rescheduling would create a path for medical marijuana. This is not the first time re-scheduling at the federal level has caused trigger laws to go into effect. In 2018, the Food and Drug Administration (FDA) approved Epidiolex, a CBD oral solution as a medical treatment for epilepsy. The federal government subsequently moved CBD to Schedule V of the CSA. After that, the manufacturer of Epidiolex, GW Pharmaceuticals, now Jazz Pharmaceuticals, was able to distribute its medication to all 50 states yet cannabis is still federally illegal. In other states, federal rescheduling would initiate a process requiring further action by the state legislature or a controlling state authority.

State Markets and EBITDA Growth

At the state level, the adult-use ramp-up in new recreational states such as Maryland and Ohio will drive industry sales growth. Florida and Pennsylvania will also move towards adult-use, which could improve sentiment as well, but actual sales in those states are likely to start in 2025. EBITDA upside for incumbent operators in states that have either recently begun recreational sales or should go recreational in the next 12 months includes MD, OH, FL, PA and VA.

MD, OH, FL, PA and VA.

Ohio

Ballot Initiative: Implementation in 2024

After the successful ballot initiative to allow recreational cannabis sales in Ohio, the state Senate passed a bill that would accelerate the opening of the commercial market, allowing medical operators to sell cannabis within 90 Days, a much shorter time frame than originally anticipated. In addition, the bill adjusts the excise tax on sales from a proposed 10% to 15%, however the bill is removing the 15% cultivation tax. Approval from both the House and Senate is required. Ohio’s medical market generated ~$470M of cannabis sales in ’22 vs PA at over $1.5 billion and relatively similar populations. Comparing Ohio to neighboring Michigan where adult-use sales are legal, with annualized cannabis sales estimated at $3 billion and fewer residents than Ohio, we believe adult-use sales could be significant for Ohio.

Also benefiting operators, Ohio’s medical market is consolidated with mostly vertically integrated MSOs and remains a limited licensed market. This is a meaningful state for the publicly traded MSOs. Given the transition to recreational, we could see OH jumping significantly as recreational results in greater format choices, reduced THC caps and changes to personal purchasing caps. Fund positions with exposure to OH include Green Thumb and Verano with a maximum of 5 stores each and Trulieve with 4.

Pennsylvania

PA is a medical market, with sales above $1.5 billion. There are 430,000 registered active patients representing 3.3% of the population, according to official state data. On a per capita basis, the PA medical market is about 10x the size of Virginia, based on the rules established by each state in terms of cultivation footprints allowed and the number of retail locations operating. With more stores and less format restrictions post recreational transitions, the market could even be bigger. In PA, the Fund's top cannabis holdings are all represented with Trulieve at 20 stores, Curaleaf at 18, Verano at 17, Green Thumb at 16, while TerrAscend at 6 retail locations. Following Ohio’s successful ballot initiative, PA is almost completely surrounded by adult-use states. Revenue loss (meaning loss of state tax revenues) as consumers buy in neighboring states will consequently become a bigger issue for politicians in PA to contend with, and we expect this will hasten PA’s path to becoming an adult-use state.

Florida

The state has a very well-publicized public process to have a ballot initiative on the November 2024 election night. The rules for the state have a high number of signatures required that were provided and submitted to the Governors office this Fall. Gov DeSantis is not a big supporter of cannabis and so there is still a political battle and court battle at the State Supreme Court prior to the vote in November. At this stage, the State Supreme Court has heard submissions from both sides of the debate and a decision is expected in early April. The Florida medical market is already one of the largest markets in the US generating sales estimated to be over $2 billion. Although the state has over 600 dispensaries, the unofficial limitation for any operator to open a store in Florida is what is called “Forced Verticalization” meaning you can only sell what you produce. There is no wholesale market, so operators need deep pockets of capital to establish a market presence and be successful. Currently, Fund holdings are represented with Trulieve being the market leader with over 130 dispensaries, followed by Verano with 73 storefronts and Green Thumb at 13. It is also important to consider that to support its retail operation, Trulieve has over 4 million sq ft of cultivation in northern Florida, and with that volume, outsells average store volumes by 3:1. The opportunity for transition to the recreational market is to remove purchasing caps, increase formats and provide broader market product differentiation. We estimate that transitioning to recreational, given annual tourism, Florida could be a $5-6 billion market.

Canadian Cannabis: The Cash Burn Continues in 2024

We continue to be significantly underweight in Canadian cannabis. Yes, the market is growing with nationwide sales over $5 billion. However, there are several factors that conspire against the current industry participants. For starters; prohibitively high federal and provincial tax rates; followed by a lack of efficient operations at the cultivation and production level leading to a lack of operating cash flow for licensed producers; at the retail level there is intense competition for storefront locations. All of the above-noted issues have contributed to a lack of profitability on the part of most players.

Despite overall sales growth in the Canadian cannabis market, profit has been elusive for many operators. It has now been five years since recreational legalization allowed consumers to have a greater choice of format in addition to the type of strains and amount of THC content. However, the major public companies continue to be mired in losses from the past five years of questionable capital spending programs. Tilray (TLRY) continues to grow top-line revenue, aided by acquisitions in low-margin alcohol and beer brands that attract lower multiples, cash flows have been reduced. Very few of the largest cannabis companies in Canada have positive cash flow. Canopy Growth (WEED) and Aurora Cannabis (ACB) still don’t make any money from Canadian cannabis and the non-cannabis brands they have acquired have not been successful either, the latest being WEED’s BIOSteel division that filed for bankruptcy protection.

Unfortunately, the Canadian cannabis sector has seen its fair share of challenging financial outcomes. To mid-December of 2023, insolvencies in the space continue with this year’s more well-known names such as cannabis retail and software provider Fire & Flower (FAF) and producer Aleafia Health (AH) both filing for bankruptcy protection. This is a continuing battle that has plagued the industry north of the border having to deal with low marijuana retail prices, high tax rates and trouble accessing capital. In 2023, 12% of companies that filed under the CCAA (Companies’ Creditors Arrangement Act) are cannabis-related businesses, representing a decline from 2022, when more than 33% of all businesses filing for CCAA were involved in the Canadian cannabis industry.

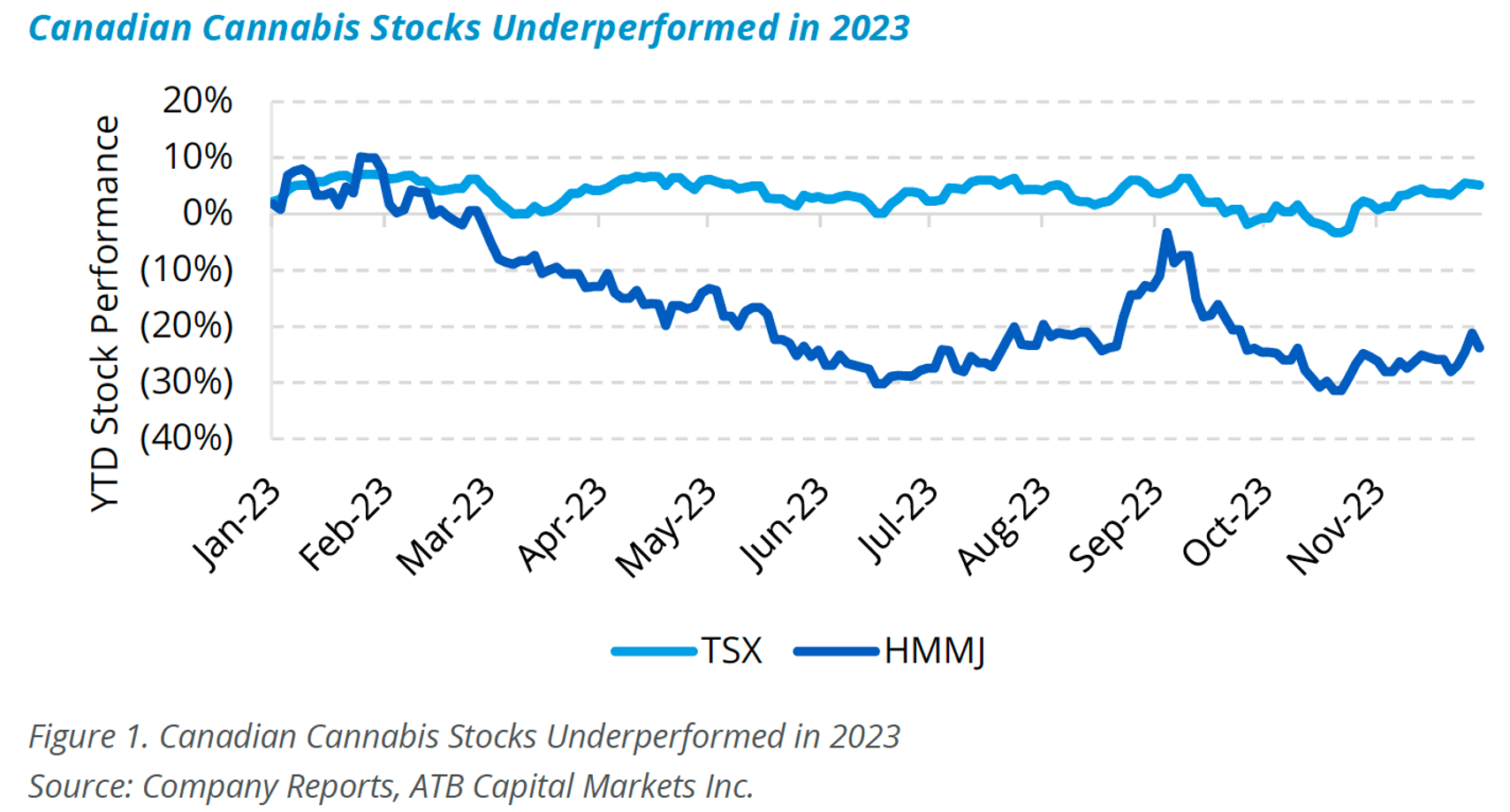

We believe that Canadian cannabis stocks will continue to underperform. There is a glut of retail locations continuing to put pressure on wholesale pricing, while provincial tax regimes continue to plague the industry. The province of Ontario has recently increased the number of dispensaries owned by an entity to 150 from 75, it remains to be seen whether this drives economies of scale or adds to further profitability strain in the largest cannabis market in the country. The retailers are beginning to generate free cash flow, and we anticipate that they will outperform the cultivation/processing companies in 2024. Overall, the industry saw growth in sales of over 10% in 2023 reaching $5 billion, however we suggest that profitability will remain elusive for much of the Canadian names.

The cultivation companies continue to focus on right-sizing cost structures, and with continued success, we expect improvement in the overall cash burn for the sector. But as the chart below illustrates, Canadian cannabis has underperformed the TSX by a wide margin in 2023, that is not something that we see changing direction in 2024.

Germany: Will 2024 Be the Year?

We continue to watch with cautious optimism as German Health Minister Karl Lauterbach attempts to enact federal cannabis laws that follow the Canadian model, creating a state licenced production and sales system, allowing homegrown plants for personal use and creating a federal cannabis tax regime. Minister Lauterbach set 2024 as a possible date for passing German legislation. There is still the matter of how Germany’s goal of national cannabis legalization sits within the European Council 2004 Framework Decision and the Schengen agreements. Those continental agreements among neighboring states require all members to maintain that cannabis is criminalized in terms of production, distribution and sale. The German proposal is attempting to use a notification system to allow Germany to stay a member in good standing. The European cannabis market has the potential to be in the several billion Euro range, but we still believe it is years away. While Europe has the potential to be a large market, the difficulties of “threading the needle” of cannabis reform while staying onside of EU law should not be underestimated. In addition, we have concerns that even if such reforms are passed, the market may end up looking like Canada – large but generally unprofitable. We continue to closely monitor developments in Europe but remain cautious for the time being.

Healthcare & Pharma Trends in 2024

While healthcare and pharma performance in 2023 was generally muted, there are a number of trends that we believe will drive the sector’s performance in 2024. Overall, we continue to see these sectors as important components of the Fund, particularly in a more uncertain economic environment. Some of the top themes we see for 2024 are detailed below.

Pharmaceuticals: GLP-1 Catalysts in 2024

We continue to see significant growth for the innovative drugs that are treating obesity and type II diabetes, and we believe that the companies leading this innovation will continue to see growth in equity value in 2024. The overall GLP-1 market is led by Novo Nordisk (NOVO) and Eli Lilly & Co (LLY). Between the two companies, they combine to distribute the five top products in the GLP-1 space, with a multi-year lead relative to latecomers such as PFE, Roche, Merck and others. We believe that GLP-1 drugs have the same effect on pharma stocks as AI has on large-cap tech stocks.

GLP-1 drugs are injectable glucose-lowering medications approved by the FDA for the treatment of adult patients for weight loss as well as the treatment of type II diabetes. A key driver of growth for the GLP-1’s in addition to delivering their primary objectives of weight loss and/or insulin level management, are the results illustrating additional health benefits in clinical trials. Clinical trial results include major additional health benefits such as reduction in major adverse cardiac events (MACE or heart attack); kidney and liver disease as well as other long term chronic health challenges such as sleep apnea. As a result, we believe that the leaders in the space, LLY and NOVO have significant upsides. There are approx. 150 million people in the US who are overweight or more severely categorized as obese. These breakthrough medications could be seen to treat 30-40% of these patients at any given time (for 3 to 6 months at a time). With respect to diabetes, over 37 million Americans have diabetes (approx. 10%), and approximately 90-95% of that group have type 2 diabetes.

The GLP-1 receptor agonist market was estimated at USD $22.4 billion in 2022, with only an estimated 2-4% penetration rate currently, relative to the total population with either obesity or type II diabetes. (source: Cowen). The market opportunity for GLP-1 drugs over the next decade has been estimated at $55 billion by Cowen to $71 billion by JP Morgan to $91 billion by 2031 by Pfizer CEO Albert Bourla when discussing PFE’s investigational oral treatment danuglipron.

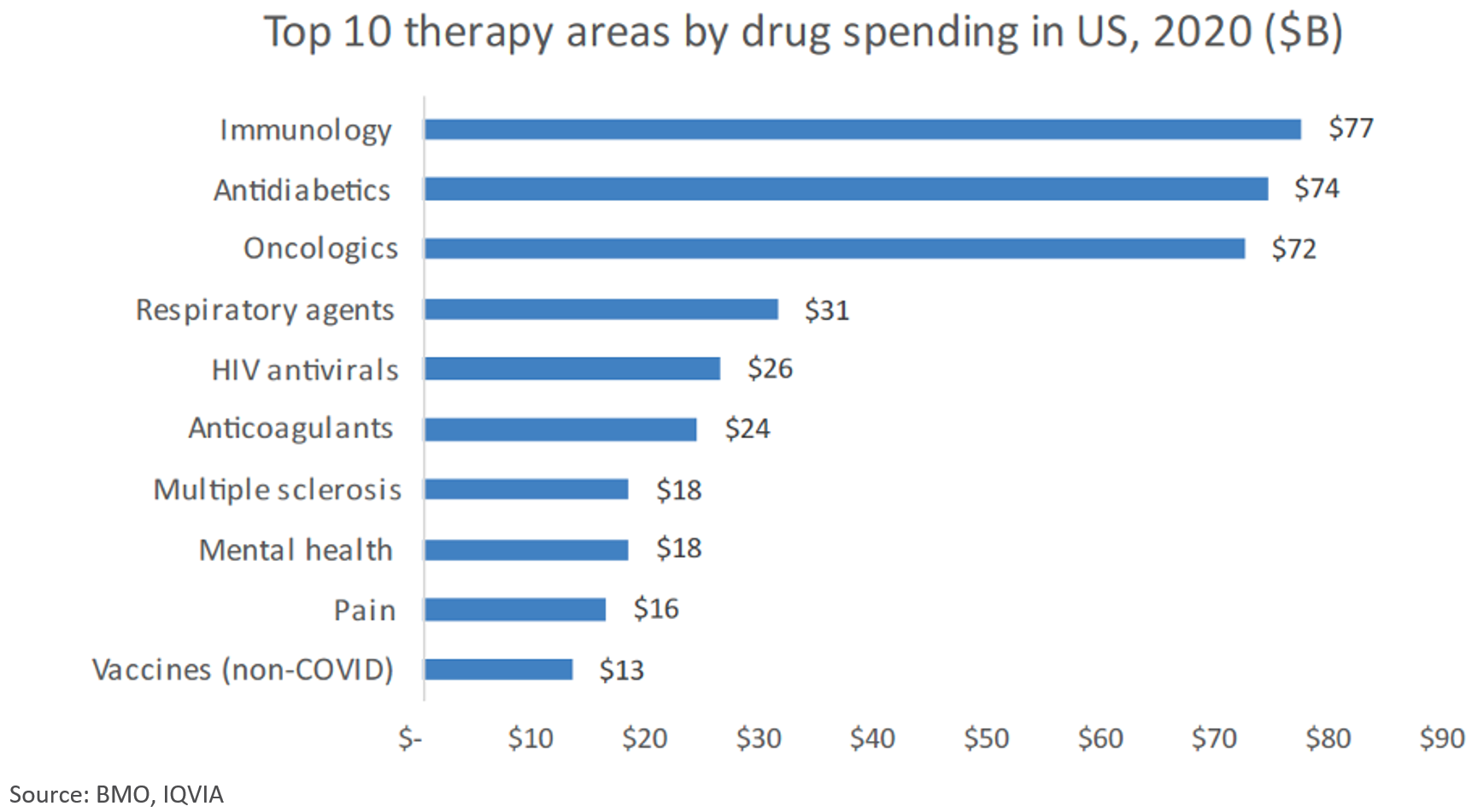

Some investors may push back on sizing the GLP-1 market for the US however it must be noted that in 2020, sales of existing anti-diabetic drugs in the US amounted to approximately $74 billion. We must also consider the potential size of this market and the current uptake in the low single digits, somewhere around 2-4% of adults who have either type II diabetes or are dealing with obesity issues. As a result, we believe it is reasonable to see market growth of these drugs both from the standpoint of replacing existing anti-diabetic treatments, but also in comparison to breakthrough drugs in other areas of the healthcare system. Examples of individual drugs with top peak worldwide revenues include Keytruda MRK (for various cancer treatments) with sales of $20.9 billion in 2022 (still growing), Eliquis from PFE and BMY (specialized blood thinner) and Humira ABBV (for various autoimmune diseases) which peaked at $21.2 billion in 2022. Lipitor PFE (cholesterol) peaked in 2006 at $12.6 billion. As a result, we see further upside for the GLP-1 providers and our top holding in the space, LLY.

Drug Spending by Therapeutic Area since 2020

Healthcare & Wellness Trends

While the clinical aspects of medicine have received a lot of headlines, access to healthcare at an affordable price remains a challenge for many people, and healthcare represents a growing share of total expenditures for many governments. We believe there are opportunities to invest in healthcare “disruptors”, successful companies from other industries that are able to apply their innovations and efficiency to the distribution of healthcare products and services. We would include companies like Walmart (WMT), COSTCO (COST) and Amazon (AMZN).

WMT has long been recognized as a disruptor in the retail space, using its size and wholesale distribution and operational efficiencies to offer superior pricing to consumers. In addition to its traditional business, WMT offers a range of healthcare products and services that attract an increasing component of its customer base. Through Walmart Health, the company also offers a pharmacy dispensary, vision care, and medical insurance in addition to a range of medical, dental, and behavioral health services. In a year where retail/consumer staples were challenged, WMT returned 12.8% in 2023.

Another large retailer that has been able to leverage its distribution and efficiency in the healthcare space is COSTCO (COST). Over the last decade, COST has substantially increased the range of healthcare products and services it offers to its members. Using its member-based warehouse channel, COST has established significant revenues from its Kirkland brand of vitamins and supplements in addition to its pharmacy; vision care services such as eye exams and dispensing of prescription lenses, as well as hearing tests. In addition, COST offers a wide variety of nutritional products. More recently, COSTCO has expanded its healthcare offering in the U.S. with access to online medical visits for $29 through a partnership with Sesame Care. Sesame is a telehealth platform that provides care for physical and mental health concerns. The platform is built to search by specific ailments or symptoms, in addition to allowing members to schedule online or in-person appointments. This is an effective way to add health related services that are driving value to members while broadening COST’s offering and deepening its relationship with its customers. COST was one of the fund's top performers in 2023, returning 52.4%.

Another company that deserves attention given their size and breadth of operation outside the traditional healthcare space that is driving innovation in healthcare services is Amazon (AMZN). AMZN acquired One Medical for US$3.9 billion in the summer of 2022, marking AMZN’s third foray into health care services. ONEM is a service that offers virtual care as well as in-person visits. It works with more than 8,000 companies that includes +760,000 members providing health benefits/services with +190 medical offices in 25 state markets. Late in 2022, AMZN then announced the establishment of Amazon Clinic which Amazon describes as a virtual health storefront addressing a variety of conditions that are some of the more broadly requested for telehealth consultations. Amazon Clinic is now available in all 50 states in the U.S. What AMZN is doing with these virtual and in-person health care services is offering different types of health services addressing different needs. One Medical focuses on a long-term patient relationship with a primary care doctor, while Amazon Clinic is intended for more “one-off” urgent care situations. For AMZN, these acquisitions deepen its health care service offerings building on its online pharmacy PillPack which it acquired in 2019. Given its balance sheet strength we believe AMZN can be an innovative disrupter to lead the next few years in terms of patient need.

Growth in Demand for Wellness Alternatives

We believe that the long-term trend towards non-dairy drinks continues to show significant upside. Future Market Insights sees the alt dairy category growing to $20 billion in sales by the end of 2023. The growth rate for alt milk had a CAGR (compound annual growth rate) of 7.8% in the last five years and is expected to grow with a CAGR of 10% over the next 10 years. This is at a time when dairy milk consumption has come off. Alt-milk’s market share of the overall milk market has increased from 5.9% in 2017 to 9.4% in 2022, based on data from IRI, a market research group. Worldwide sales of alt-milks are growing steadily, driven by several drivers; chronic lifestyle diseases such as heart disease, type 2 diabetes and chronic kidney disease; a growing recognition of lactose intolerance, in addition to a global goal to reduce the environmental impact related to dairy farming.

On the health front, research released in Lancet back in 2017, estimated that approx. 66% of the global population is unable to digest or fully digest lactose, a sugar found in milk. Lactose intolerance is most common in Asia, the Middle East and Africa and to meet that demand plant-based milks contain no lactose. While milk producers have come out with lactose free milk, those account for 7% of overall milk sales while alt-milks are over 11% of the overall market for milk and alt milk consumption. We believe alternative milk producers such as Sunopta (STKL) are set to benefit from this trend.

The Ninepoint Alternative Health Fund, launched in March of 2017 is Canada’s first actively managed mutual fund with a focus on the cannabis sector and remains open to new investors, available for purchase daily.

Charles Taerk & Douglas Waterson

The Portfolio Team

Faircourt Asset Management

Sub-Advisor to the Ninepoint Alternative Health Fund

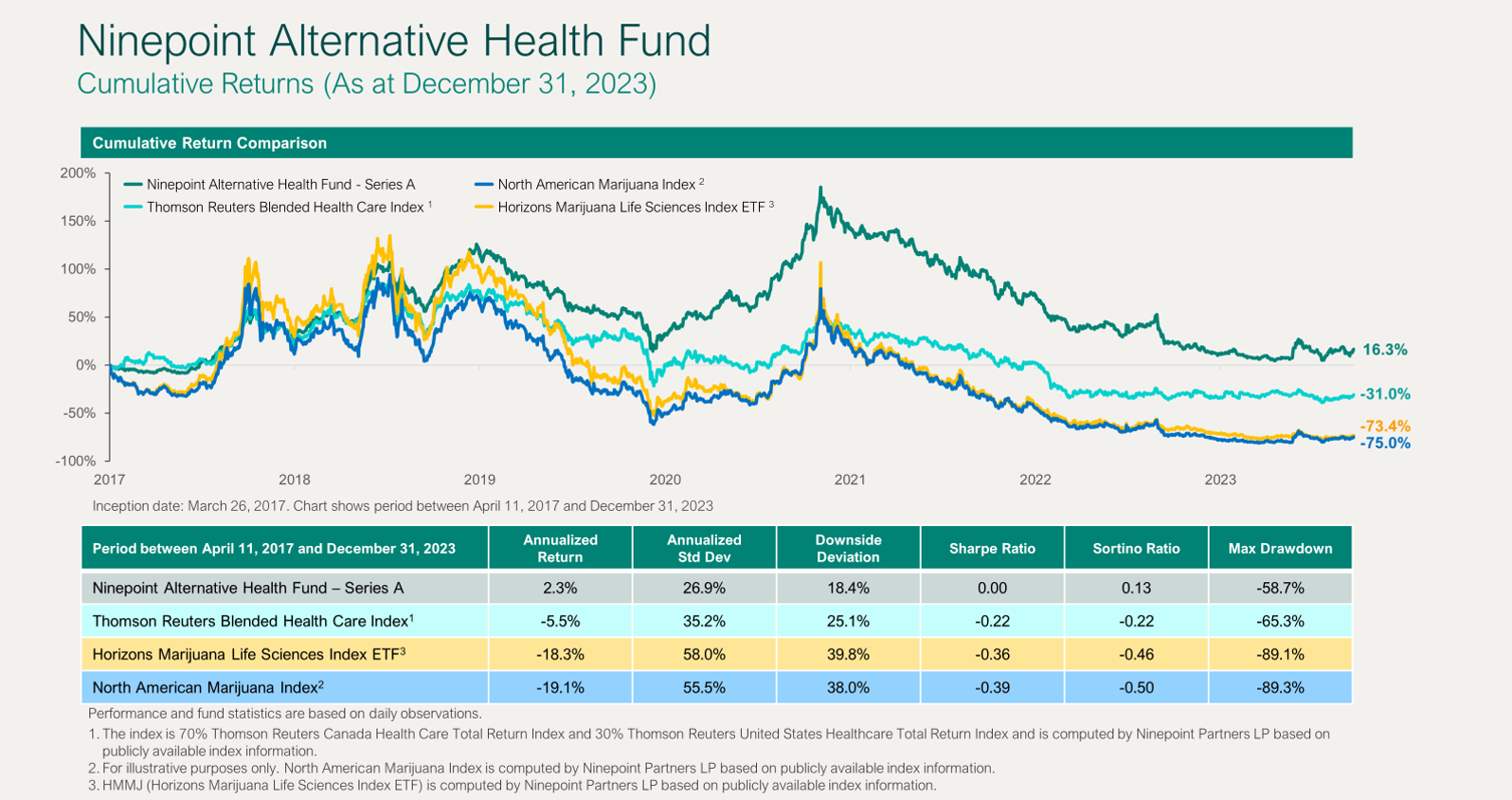

Ninepoint Alternative Health Fund - Compounded Returns¹ as of December 31, 2023 (Series F NPP5421) | Inception Date - August 4, 2017

| MTD | YTD | 3MTH | 6MTH | 1YR | 3YR | 5YR | INCEPTION (ANNUALIZED) |

|

|---|---|---|---|---|---|---|---|---|

| FUND | 0.5% | -5.1% | -1.7% | 7.5% | -5.1% | -17.1% | -5.7% | 4.2% |

| TR CAN/US HEALTH CARE BLENDED INDEX | 5.4% | 5.4% | 0.6% | 0.1% | 5.4% | -14.8% | -12.6% | -6.2% |

Statistical Analysis

| FUND | TR CAN/US HEALTH CARE BLENDED INDEX | |

|---|---|---|

| Cumulative Returns | 30.6% | -33.7% |

| Standard Deviation | 27.1% | 28.7% |

| Sharpe Ratio | 0.07 | -0.30 |

1 All returns and fund details are a) based on Series F units; b) net of fees; c) annualized if period is greater than one year; d) as at December 31, 2023. The index is 70% Thomson Reuters Canada Health Care Total Return Index and 30% Thomson Reuters United States Healthcare Total Return Index and is computed by Ninepoint Partners LP based on publicly available index information.

The Fund is generally exposed to the following risks. See the prospectus of the Fund for a description of these risks: Cannabis sector risk; Concentration risk; Currency risk; Cybersecurity risk; Derivatives risk; Exchange traded fund risk; Foreign investment risk; Inflation risk; Market risk; Regulatory risk; Securities lending, repurchase and reverse repurchase transactions risk; Series risk; Specific issuer risk; Sub-adviser risk; Tax risk.

Ninepoint Partners LP is the investment manager to the Ninepoint Funds (collectively, the “Funds”). Commissions, trailing commissions, management fees, performance fees (if any), and other expenses all may be associated with investing in the Funds. Please read the prospectus carefully before investing. The indicated rate of return for series F shares of the Fund for the period ended December 31, 2023 is based on the historical annual compounded total return including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Fund may be lawfully sold in their jurisdiction.

The opinions, estimates and projections (“information”) contained within this report are solely those of Ninepoint Partners LP and are subject to change without notice. Ninepoint Partners makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Ninepoint Partners assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Ninepoint Partners is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Ninepoint Partners. Any reference to a particular company is for illustrative purposes only and should not to be considered as investment advice or a recommendation to buy or sell nor should it be considered as an indication of how the portfolio of any investment fund managed by Ninepoint Partners is or will be invested. Ninepoint Partners LP and/or its affiliates may collectively beneficially own/control 1% or more of any class of the equity securities of the issuers mentioned in this report. Ninepoint Partners LP and/or its affiliates may hold short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, Ninepoint Partners LP and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

Ninepoint Partners LP: Toll Free: 1.866.299.9906. DEALER SERVICES: CIBC Mellon GSSC Record Keeping Services: Toll Free: 1.877.358.0540

Investment Team

Related Funds

Historical Commentary

- Alternative Health Fund 11/2023

- Alternative Health Fund 10/2023

- Alternative Health Fund 09/2023

- Alternative Health Fund 08/2023

- Alternative Health Fund 07/2023

- Alternative Health Fund 06/2023

- Alternative Health Fund 05/2023

- Alternative Health Fund 04/2023

- Alternative Health Fund 03/2023

- Alternative Health Fund 02/2023

- Alternative Health Fund 01/2023

Toronto, Ontario M5J 2J1 Canada